5-year term life insurance is a popular, budget-friendly form of temporary life insurance in Canada. With guaranteed premiums and death benefit payouts for 5 years, it provides financial protection for your family during short-term needs or as a supplement to permanent policies.

However, is it the right choice for you? This guide offers an in-depth look at 5-year term life insurance in the Canadian market. Whether you are a first-time buyer or reviewing your existing coverage, use this guide to make a truly informed decision.

Key Takeaways:

- 5-year terms offer the lowest initial premiums, but the highest increases in premiums when renewal

- Average cost: $15-$200/month, depending on age, health, and coverage amount

- Renewable until age 75-80; convertible to permanent insurance without a medical exam

- Best for temporary debts, transitional life stages, budget-conscious consumers…

- Not ideal for permanent needs, estate planning, those over 60…

What is 5-Year Term Life Insurance?

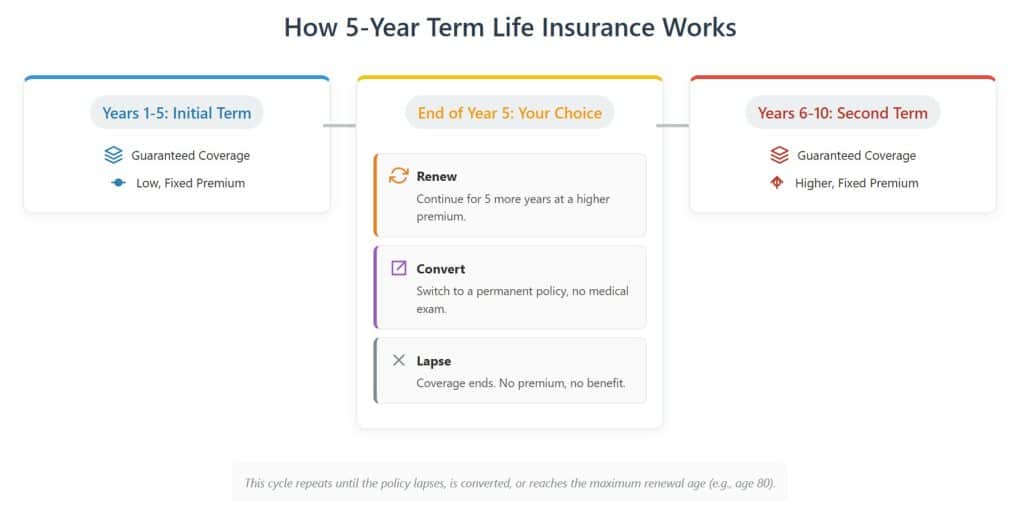

A 5-year term life insurance policy is a contract that provides a tax-free, lump-sum death benefit to your beneficiaries if you pass away during the 5-year term. During these five years, the insurer cannot cancel your policy or raise your premiums, even if your health declines. This provides certainty and peace of mind.

At the end of the term, you have the option to renew for another 5 years without proving your health status. However, this renewal comes at a significantly higher premium based on your new age. Most policies allow renewals until an age limit, usually 75 to 80. Furthermore, many policies include a crucial conversion privilege, allowing you to convert your term policy into a permanent policy (like Whole Life or Universal Life) without a new medical exam.

The death benefit provides tax-free funds to pay funeral costs, debts like mortgages, daily living expenses and more. This can help protect families from financial hardship if a wage-earning spouse or parent dies prematurely

How It Differs from Other Terms

| Policy Type | Initial Cost | Renewal Frequency | Best For |

|---|---|---|---|

| 5-Year Term | Lowest | Every 5 years | Very short-term needs (under 5 years) |

| 10-Year Term | Low | Every 10 years | Medium-term needs (5-10 years) |

| 20-Year Term | Moderate | Every 20 years | Long-term needs (child-rearing, mortgage) |

| Permanent | Highest | None (lifelong) | Estate planning, lifetime protection |

What to Do When Your 5-Year Term Ends

At the end of your term, you face a critical decision. Do not simply let the policy auto-renew without exploring your options.

- Renew: Only do this if your health has significantly worsened and you can no longer qualify for a new policy. The renewal premium will be high, but it guarantees you remain covered.

- Convert: If your need for insurance has become permanent and your health has declined, convert a portion (or all) of your term policy to a permanent one. You will lock in lifelong coverage without a medical exam.

- Reapply: If you are still in good health, this is almost always your best option. Shop the market for a brand new term policy (whether 5, 10, or 20 years). Your new premiums, based on your current age and good health, will be far lower than the renewal premium of your old policy.

Advantages of 5-Year Term Life Insurance

There are 5 advantages that make 5-year term insurance policies a popular choice in Canada:

Lower Premiums

The primary advantage of a 5-year term is its affordability. With no cash value accumulation, term life insurance generally has more affordable premiums, especially for shorter 5 or 10-year terms. This allows you to secure a large death benefit for a minimal cost.

Coverage When It’s Needed Most

The policy provides protection during a specific period when your dependents would need it most in the event of your death. You can match it to the years when coverage is essential, such as when children are young or debts are outstanding. Because the premiums are lower due to the short term, you may also be able to afford a higher coverage amount during this crucial period.

Flexibility and Re-evaluation

Life circumstances tend to change over time. After 5 years, your income may have grown, your mortgage may have shrunk, or your children may have become more independent. You can reassess your coverage needs and adjust accordingly.

Guaranteed Insurability via Conversion Options

If you develop a health condition like diabetes or heart disease during your term, you might become uninsurable on the open market. Many 5-year term policies allow converting to permanent life insurance without a medical exam before renewal. This privilege allows you to secure lifelong coverage regardless of your new health status.

Disadvantages of 5-Year Term Life Insurance

While there are benefits, drawbacks should also be considered when evaluating a 5-year term life insurance policy:

The Renewal Trap

This is the single biggest drawback. The coverage expires after 5 years if the policy is not renewed. While you can renew, the premiums will increase dramatically. Relying on renewals for long-term needs is an expensive strategy.

So, it’s critical to assess how long you anticipate needing coverage accurately. If you underestimate this duration, your loved ones could end up uninsured.

Not Ideal for Long-Term Needs

For long-term needs such as final expenses, estate planning, or leaving a lifelong legacy, a 5-year term is generally not the best option. If your need for insurance extends beyond 5-10 years, a longer term (e.g., 20-year term) or permanent policy is likely more cost-effective in the long run.

No Cash Value

There is no savings or investment component, unlike permanent life insurance plans. Any premiums paid into the policy provide pure insurance protection only. This means if you cancel the policy during the 5-year term, you would not get any monetary value back. With permanent insurance, you’d at least get your accumulated cash value returned.

For temporary needs under 5 years, these downsides may be less concerning, but they should be carefully evaluated based on your specific situation and coverage needs.

Who Might Want 5-Year Term Life Insurance?

While longer-term policies are more common, a 5-year term is ideal for specific financial situations and life stages. It’s a strategic tool for precise, short-term protection. Here are some scenarios where it makes the most sense:

Individuals with Short-Term Financial Obligations

If you have a debt that you plan to pay off within 5 years, such as a vehicle loan, student loan, small mortgage, or personal loan, a 5-year term policy can provide coverage just for that period.

Budget-Conscious Individuals or Families

For young families just starting out, finances can be tight. A 5-year term offers the lowest possible premium, providing essential protection during the early years when it’s needed most. The strategic plan can be to convert the policy or purchase a longer-term one once income increases and the budget allows for it.

People Between Jobs or Careers

If you are in between jobs or switching careers, a 5-year term policy can provide temporary coverage until you get established. The lower cost of 5-year term insurance allows you to maintain coverage during a transitional career stage.

Those Nearing Retirement

For those in the final stretch before retirement (e.g., 5-7 years away), a 5-year policy can provide crucial peace of mind. It can cover the last few years of income-earning, ensuring a spouse or partner is financially secure until pensions, Social Security, and retirement savings become fully accessible.

New Parents

Many parents choose a 5-year term to cover the initial few years until their children reach school age and reduce their dependency. Once the kids grow older, the coverage needs and costs may change. So, a short 5-year term allows new parents to match their life insurance coverage to the periods they feel are essential.

People Expecting Health or Lifestyle Improvements

If you’re currently a smoker who plans to quit or are recovering from a medical condition, your insurance rates might be high. You could purchase an affordable 5-year policy to have coverage now, with the goal of reapplying for a longer, cheaper policy in a few years once your health profile has improved and you can qualify for a better rate class.

5-Year Term vs. 10-Year Term: Making the Right Choice

For many Canadians, the choice isn’t between term and permanent, but between different term lengths. The 5-year and 10-year terms are two of the most common choices for short-term needs.

A 10-year term policy will have a higher monthly premium than a 5-year term for the same coverage amount. However, that premium is guaranteed to stay level for a full decade. This provides cost certainty and stability.

The crucial factor is the breakeven point. A 5-year term is cheaper for the first five years. But if you need coverage for year six and beyond, you must renew the 5-year policy at a much higher rate based on your older age. In most cases, the total cost of paying for a 5-year term and then renewing it for another five years is significantly more expensive than simply buying a 10-year term from the start.

- Choose a 10-year term if: You are confident your need for coverage will last at least 6-10 years. This is common for parents with young children or those with a mortgage that has more than 5 years remaining. It offers better value and peace of mind over the medium term.

- Choose a 5-year term if: Your need is definitely short-term or your financial situation is currently uncertain, and the absolute lowest initial premium is your top priority.

Case Study: When a 5-Year Term is the Perfect Fit

William is a 32-year-old marketing manager with a young child and a mortgage. He has decided to leave his corporate job to pursue a 2-year Master’s degree, after which he plans to launch her own consulting business. His group life insurance from his employer will end when he resigns.

The challenge: William needs to replace his life insurance to protect his family, but his income will decrease while he studies and then slowly builds his business for the next few years. He cannot commit to the higher premiums of a 20-year term or permanent policy right now.

The solution: William works with an advisor and chooses a $750,000 5-year term life insurance policy.

Why it Works:

The 5-year term premium is the lowest available, fitting comfortably within his tight student budget while still providing a substantial death benefit to cover the mortgage and the child’s needs. The 5-year term also perfectly bridges his period of uncertainty. It covers the two years in school and the first three crucial years of establishing his business.

In five years, at age 37, his business should be profitable and her income stable. At that point, he can reapply for a new policy, perhaps a 20-year term, that reflects his new financial reality. This new policy, while at a 37-year-old’s rate, will be far cheaper than renewing her original 5-year term.

In addition, if William were to be diagnosed with a serious illness during her 5-year term, he could convert the policy to permanent coverage without any medical questions, guaranteeing his family’s long-term protection.

Therefore, for William, the 5-year term isn’t a permanent solution; it’s a strategic, low-cost bridge to a more stable future.

How Much Does 5-Year Term Life Insurance Cost?

The cost of term life insurance depends on your age, gender, smoking status, coverage amount, and, most importantly, your health classification.

- Age: Younger ages qualify for lower premiums, as mortality risk increases as you age. Rates start rising around age 40 and increase more sharply at age 50 and beyond.

- Gender: Due to differing life expectancy, premium rates are lower for women than men at younger ages, but even out by the 50s and 60s.

- Health: Any medical conditions you have or lifestyle risks will result in higher premiums compared to healthy individuals. Insurers typically use classes like Super Preferred (excellent health), Preferred (very good health), and Standard (average health).

- Occupation: High-risk jobs (mining, piloting, fishing) add a 10-50% surcharge

- Coverage amount: The higher the death benefit you purchase, the higher the required premiums to fund the policy.

- Term Length: Premiums are lower for shorter 5- or 10-year terms than for longer 15-, 20-, or 30-year terms.

Here are sample monthly costs for 5-year term life insurance by age and coverage amount:

| Age | $250,000 Coverage | $500,000 Coverage | $1,000,000 Coverage |

|---|---|---|---|

| 25 | $16 | $27 | $48 |

| 35 | $19 | $33 | $60 |

| 45 | $30 | $50 | $90 |

| 55 | $100 | $160 | $280 |

| 65 | $195 | $310 | $540 |

Premiums can also vary slightly by province. Rates are generally most affordable in Quebec, followed by Ontario, with Manitoba and Atlantic provinces being more expensive.

Read more: Strategies for Lowering Your Term Life Rates

Who Are the Top 5-Year Term Life Insurance Providers in Canada?

When comparing insurers, look at premium rates, underwriting process, ability to bundle with other policies, online servicing capabilities, and financial strength ratings.

Below are 5 of the top providers of term life insurance in Canada to consider:

Sun Life Financial

- Offers renewable and convertible 5-year term life insurance

- Available for ages 18-80

- Death benefit amounts up to $50 million

- Can add optional critical illness and disability insurance

- Online instant quote calculator

Best for: High coverage amounts and integrated solutions. Sun Life is a giant with immense financial strength and can handle very large face amounts (into the millions). They are competitive for young, healthy applicants and offer excellent optional riders like Critical Illness coverage.

Read the full review: Sun Life Insurance Canada

Canada Life

- Affordable 5-year term life insurance plan

- An option for the 10-year renewable term is also available

- Can add critical illness and disability insurance

- Access to Best Doctors services

- Policies available entirely online

Best for: Simplicity and digital experience. Canada Life has invested heavily in a smooth online application process. Their term products are straightforward and competitively priced, making them a great choice for those who value a simple, no-fuss approach.

Read the full review: Canada Life Insurance

RBC Life Insurance

- A 5-year term life policy can be renewed annually up to age 90

- Option to convert to RBC permanent life insurance

- Add AD&D rider

Best for: Convenience for existing RBC clients. RBC offers the ability to bundle insurance with your banking products. While their rates may not always be the absolute lowest on the market, the convenience and ease of management through a familiar institution are major draws for their customers.

Read the full review: RBC Life Insurance

BMO Insurance

- 5-year renewable term life insurance policy

- Tailored for mortgage protection needs

- Must be a BMO banking client to apply

Best for: Applicants with minor health concerns. BMO is known in the brokerage community for its more lenient underwriting on certain health conditions. If you’ve been declined or rated poorly elsewhere, BMO may offer a more favourable outcome.

Read the full review: BMO Life Insurance

Manulife Financial

- 5-year term life insurance can be renewed annually until age 105

- No medical exam is required for renewals

- Conversion available to a Manulife permanent life insurance policy

- Access to the Manulife Vitality program

Best for: Healthy, active individuals. Their Vitality Program offers premium discounts and rewards for maintaining a healthy lifestyle. Their conversion options are also very robust.

Read the full review: Manulife Life Insurance

You can buy policies directly from these major insurance companies or consider using a life insurance broker. Independent brokers can shop rates from a large network of insurers to find you the most competitive pricing. They also provide personalized advice on the right policy and coverage for your needs. Most offer online quotes as well.

Tips for Buying 5-Year Term Life Insurance

If you determine a 5-year term policy may suit your short-term insurance needs, here are 9 helpful tips for purchasing the right coverage:

Compare Quotes Extensively

Rates for the same applicant and coverage amount can vary dramatically between insurers. Get quotes online through insurance marketplaces. An independent broker can also provide you with shop rates from multiple companies.

Calculate the Right Coverage Amount

Too much coverage adds unnecessary cost, while too little leaves your family underinsured. Consider all debts, income to replace, funeral costs, family expenses, and don’t just take the maximum amount.

Consider Optional Riders

Riders like critical illness insurance, disability insurance, and dependent children coverage can enhance a term life insurance policy for minimal added cost.

Read the Fine Print

Understand the policy renewals, conversions, exclusions, limitations, clauses for qualifying events like suicide, and other details of the contract. An advisor can explain these clearly.

Lock In Young, Healthy Rates

Buy your initial policy when you’re young and healthy to secure the lowest premiums. Rates increase as you age and renew terms.

Maintain a Healthy Lifestyle

Your health, as well as any lifestyle factors like smoking, will be re-assessed if renewing after the 5-year term. Keeping your health on track can help ensure renewal eligibility.

Work With an Advisor

An independent life insurance advisor provides guidance to ensure this policy truly aligns with your insurance needs, both now and in the future.

Review Financial Strength Ratings

When selecting an insurer, review ratings from firms like A.M. Best that assess the company’s financial strength and ability to pay claims.

Bundle for Added Savings

You can often save more when bundling your term life policy with home, auto or other insurance policies from the same provider.

There are also longer-term options to consider. Read our valuable articles about Term 10 life insurance, Term 20 life insurance, Term 30 life insurance, Term 40 life insurance, Term 25 life insurance, and Term to Age 65 life insurance to understand the differences in cost, coverage duration, conversions, and best uses for each policy term length.

Summary

A 5-year term life insurance policy is a highly effective and affordable tool for managing short-term financial risks. Its low cost and flexibility make it ideal for young families, new homeowners, and anyone in a period of financial transition.

Working with an experienced advisor is the best way to ensure you select the coverage that truly aligns with your family’s needs and long-term financial security.

Frequently Asked Questions

What medical tests are required for 5-year term life insurance?

For policies under $500,000, you may only need to complete a questionnaire if you are under age 50. Over $500,000 or age 50+ may require a paramed exam, bloodwork and doctor records.

Why is 5-year term life insurance cheaper than permanent insurance?

Term life premiums are lower because the policy only pays out if you die within five years. Permanent insurance lasts your entire life, so premiums are higher.

When should I renew my 5-year term life insurance policy?

You'll receive a renewal notice before your term expires. Renew at least 30 days in advance to avoid a lapse in coverage. You can renew until age 75-80 depending on insurer.

Can I convert my 5-year term life policy to permanent insurance?

Most term life policies allow you to convert to a permanent life insurance policy within a conversion period, often 10-15 years from the issue date, without new underwriting.

Do 5-year term life insurance premiums go up every renewal?

Yes, premiums increase at each 5-year renewal as you enter a new age band. Renewing young and healthy keeps premiums lower over time.

Is a medical exam required to renew 5-year term life insurance?

You may need to provide an updated medical history or undergo new underwriting at renewal. Good health keeps renewal costs lower.

Can I renew my 5-year term policy after age 75?

Most insurers stop renewals at 75-80 years old. Some allow renewals to age 90 but with significantly higher premiums.

How long does it take to get approved for 5-year term life insurance?

Approval can take 1-2 weeks with simplified underwriting. It may take 4-6 weeks if a full medical exam and records are required.

Can I get a 5-year term life insurance quote online?

Yes, you can get quotes on insurer websites or use online insurance brokers to compare rates from multiple companies.

Who needs to be my beneficiary for 5-year term life insurance?

You can name any person or entity as your beneficiary. Common choices are spouses, children, parents, trusts, or charities.

What conditions disqualify you from 5-year term life insurance?

Serious conditions like cancer, heart disease and stroke may disqualify you from term life insurance or lead to higher premiums.

Can I renew my 5-year term life policy if I develop a health condition?

As long as you continue paying premiums, the insurer cannot cancel your term policy even if your health declines.

Is a 5-year term life insurance payout taxable income for beneficiaries?

No, life insurance death benefit payouts are not considered taxable income. Beneficiaries receive the full payout tax-free.

Can I get 5-year term life insurance after age 65?

It becomes difficult to qualify after 65 due to age and health. Some final expense policies are available but with higher costs.

Is there a grace period if I miss a 5-year term life premium payment?

You usually have a 30-day grace period after a missed payment before the policy lapses. Make sure to pay before the grace period ends.

Can I deduct 5-year term life insurance premiums from my taxes?

Unfortunately, term life insurance premiums are not tax deductible in Canada, unlike some permanent cash-value life insurance policies.

Article Sources:

To fully appreciate our rigorous adherence to veracity, transparency, and editorial independence, consider reviewing our Editorial Policy at Lifebuzz.ca.