As a cornerstone of Canadian conservative investing, Guaranteed Investment Certificates (GICs) provide guaranteed returns while protecting your principal investment. Though they typically offer lower returns than market-based investments, their guaranteed nature makes them ideal for emergency funds, short-term financial goals, and as stability components within diversified portfolios.

What is a Guaranteed Investment Certificate (GIC)?

A GIC, is a secure investment product offered by Canadian banks, credit unions, and trust companies, providing a guaranteed rate of return over a fixed period.

GICs offer principal protection, meaning your initial investment amount is fully protected while generating predictable interest income. GICs function essentially as loans to financial institutions, where you receive interest payments in exchange for keeping your money deposited for a specific term.

This principal protection is what distinguishes GICs from most other investment types and makes them particularly appealing to conservative investors. Unlike stocks or mutual funds, where your initial investment can decrease in value, GICs guarantee that you’ll get back at least 100% of your original deposit, regardless of market conditions. Thus, they are particularly attractive for risk-averse investors seeking stability in their portfolio.

How Do GICs Work in Canada?

GICs work through a straightforward system where you deposit funds with a financial institution for a predetermined period, during which you earn interest at an agreed-upon rate. When you purchase a GIC, you’re entering into a contract with the financial institution, committing your money for a specific term in exchange for guaranteed returns. Now let’s explore the investment requirements, interest rate factor, and what CDIC insurance protection is within a GIC.

Investment requirements

Most financial institutions require a minimum deposit of $500 to purchase a GIC, though some products may require higher minimums of $1,000 or more. There is typically no maximum limit to how much you can invest in GICs, though CDIC insurance only covers up to $100,000 per depositor per CDIC member institution for each insured category.

Interest rate factors

GIC terms range from as short as 30 days to as long as 10 years. During this contracted period, your money remains invested with the financial institution. The length of the term significantly impacts the interest rate you’ll receive, with longer terms generally offering higher rates to compensate for the extended commitment. Other factors determine the interest rate on a GIC:

- Investment amount – Larger deposits may qualify for premium rates

- Type of GIC – Non-redeemable GICs generally offer higher rates than redeemable ones

- Current economic environment – Prevailing interest rates affect GIC rates

- Financial institution – Rates vary between banks, credit unions, and trust companies

CDIC Insurance Protection

One of the most significant advantages of GICs is their eligibility for CDIC insurance. This federal crown corporation protects eligible deposits at member financial institutions for up to $100,000 per depositor, per insured category.

This means that if the bank or trust company fails, your investment (principal and interest) is protected up to this limit. Credit unions offer similar protection through provincial deposit insurance corporations.

| CDIC Coverage Categories | Maximum Insurance Coverage |

|---|---|

| Individual accounts | $100,000 |

| Joint accounts | $100,000 per set of ower |

| RRSP accounts | $100,000 |

| TFSA accounts | $100,000 |

| RRIF accounts | $100,000 |

| Trust accounts | $100,000 per beneficiary |

What Are the Different GIC Terms Available?

GICs are available in a wide range of terms, from extremely short-term options to multi-year commitments:

Short-Term GICs

Short-term GICs have maturities of less than one year, ranging from 30 days to 364 days. These products provide a balance between liquidity and returns that exceed typical savings accounts.

Short-term GICs typically offer lower interest rates than longer-term options but allow you to access your funds sooner. They’re particularly useful for:

- Parking funds you’ll need in the near future

- Building an emergency fund with slightly better returns than savings accounts

- Creating a GIC ladder (a strategy involving staggered maturities)

- Waiting for interest rates to rise before committing to longer terms

Many financial institutions offer special short-term GIC products, such as 100-day GICs with promotional rates, to attract new deposits.

Long-Term GICs

Long-term GICs have maturities of one year or longer, commonly available in 1, 2, 3, 4, 5, 7, and 10-year terms. These products offer higher interest rates in exchange for the extended commitment of your funds.

The relationship between term length and interest rate is typically direct – the longer the term, the higher the rate. However, this relationship is influenced by the yield curve, which reflects market expectations about future interest rates. If the market expects rates to fall, longer-term GICs might offer only marginally better rates than shorter-term options.

Long-term GICs are well-suited for:

- Predictable long-term financial goals

- Creating stable, guaranteed income streams

- Conservative portions of retirement portfolios

- Funds not needed for several years

The term you choose significantly impacts the interest rate and liquidity of your GICs. Understanding the different term options will help you align your GIC investment with your financial timeline and goals.

What Are the Different Types of GICs?

GICs come in various types to suit different investor needs and financial goals. Understanding these different classifications will help you select the most appropriate GIC for your situation.

The major classifications of GICs include redemption options, interest rate structures, and currency options. Each category offers distinct advantages depending on your financial circumstances and goals.

GIC Types Based on Redemption Options

GICs are primarily categorized based on their redemption flexibility, offering different levels of access to your funds during the investment term.

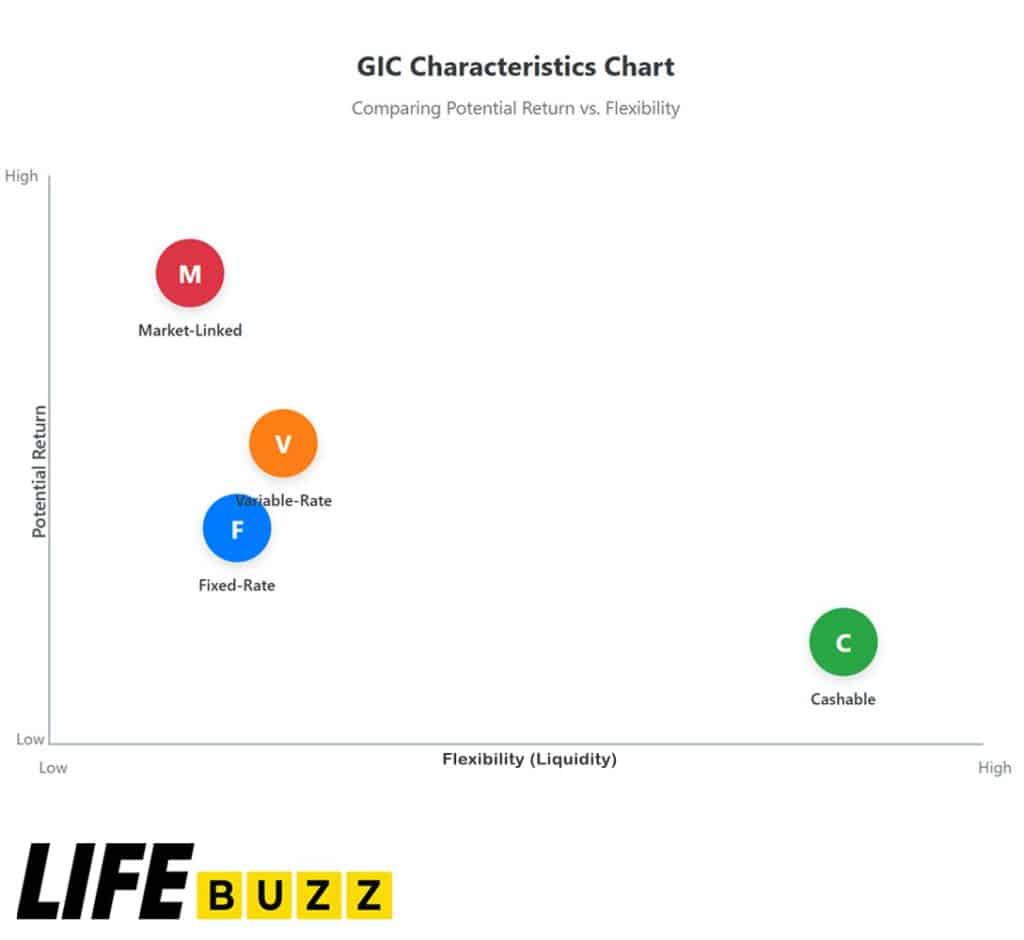

Cashable/Redeemable GICs

Cashable or redeemable GICs allow investors to withdraw their funds before the maturity date without significant penalties. These GICs provide flexibility if you might need access to your money before the term ends.

Cashable GICs typically come with a “closed period” (usually 30-90 days) during which you cannot withdraw your funds. After this period, you can cash out your investment without penalty, though you’ll receive the interest that has accrued up to the withdrawal date.

The main tradeoff for this flexibility is a lower interest rate compared to non-redeemable alternatives.

Non-Redeemable GICs

Non-redeemable GICs lock in your investment for the full term with no option for early withdrawal without significant penalties. In exchange for this commitment, they offer higher interest rates than redeemable options.

If you need to access your funds before maturity, you may face substantial penalties, including the forfeiture of all or most of the interest earned. Some financial institutions may not allow early redemption under any circumstances.

Non-redeemable GICs are ideal for investors who:

- Have a clear investment timeframe

- Don’t anticipate needing the funds before maturity

- Want to maximize their guaranteed return

GIC Types Based on Interest Rate Structure

GICs also vary based on how their interest rates are determined and applied throughout the term.

Fixed-Rate GICs

Fixed-rate GICs offer a guaranteed interest rate that remains constant throughout the entire term of the investment. This makes them highly predictable, as you’ll know exactly how much interest you’ll earn by the maturity date.

Fixed-rate GICs are particularly attractive in high-interest-rate environments or when rates are expected to fall, as they allow you to lock in favourable rates for the entire term.

Variable-Rate GICs

Variable-rate GICs feature interest rates that fluctuate based on changes in a reference rate, typically the financial institution’s prime rate. As the Bank of Canada adjusts its policy rate, banks adjust their prime rates accordingly, which directly affects the interest earned on variable-rate GICs.

The appeal of variable-rate GICs lies in their potential to benefit from rising interest rates. If rates increase during your investment term, your GIC’s returns will also increase. However, the reverse is also true – if rates fall, your returns will decrease.

These GICs are typically a good choice when interest rates are low but expected to rise during your investment term.

Market Growth GICs

Market growth GICs (also known as market-linked or indexed GICs) offer returns tied to the performance of market indices, such as the S&P/TSX Composite Index or specific securities. These hybrid products aim to provide the security of principal protection with the potential for higher returns based on market performance.

Key features of market-linked GICs include:

- Principal guarantee: Your initial investment is fully protected

- Minimum return: Many offer a guaranteed minimum return (often 0%)

- Maximum return: Returns are typically capped at a predetermined percentage

- Market correlation: Returns are linked to the performance of specified market indices

These products attempt to offer “the best of both worlds”, the safety of traditional GICs with some exposure to potential market upside. However, they often come with more complex terms and conditions than standard GICs.

How Can You Hold GICs?

GICs can be held in various types of accounts, each with different tax implications and benefits. The 2 main options include registered accounts and non-registered accounts.

Registered Account Options

Registered accounts offer tax advantages for GIC investors, but come with specific rules and contribution limits.

Tax-Free Savings Account GICs

GICs held within a Tax-Free Savings Account (TFSA) provide tax-free growth and withdrawals. Introduced in 2009, TFSAs allow Canadians to earn investment income without paying taxes on the returns.

TFSA GICs are particularly advantageous for individuals who:

- Are in higher tax brackets

- Want to maintain withdrawal flexibility

- Have maxed out their RRSP contributions

- Are you saving for medium-term goals

Registered Retirement Savings Plan (RRSP) GICs

RRSP GICs combine the security of guaranteed investments with the tax advantages of retirement savings plans. When you purchase a GIC within an RRSP, you receive:

- Tax deductions for your contributions

- Tax-deferred growth on your investments

- Potential tax savings if you withdraw in retirement at a lower tax rate

RRSP GICs are well-suited for:

- Long-term retirement savings

- Investors in higher tax brackets seeking immediate tax deductions

- Conservative portions of retirement portfolios

- Reducing portfolio volatility as retirement approaches

First Home Savings Account GICs

The home savings account introduced in April 2023 offers a unique combination of tax benefits for first-time home buyers. GICs held within an FHSA provide:

- Tax deductions on contributions (like an RRSP)

- Tax-free withdrawals for qualifying home purchases (like a TFSA)

- Annual contribution limit of 8,000, with a lifetime limit of 40,000

- Requirement to use funds for home purchase within 15 years of account opening

FHSA GICs are ideal for Canadians who:

- They are saving for their first home purchase

- Want to maximize tax advantages

- Have a timeline of less than 15 years for home purchase

- Prefer guaranteed returns for their home down payment funds

Non-Registered GICs

Non-registered GICs are held outside of tax-advantaged accounts and offer maximum flexibility but without tax benefits.

Interest earned on non-registered GICs is fully taxable as income in the year it is earned or paid, depending on the GIC type. This means you’ll need to report this interest on your annual tax return, even if you haven’t yet received the payment (for certain types of GICs).

Non-registered GICs are appropriate for:

- Investors who have maxed out their registered account contribution room

- Situations requiring amounts beyond registered account limits

- Cases where maximum flexibility is needed

- Part of a larger tax-efficient investment strategy

The account structure you choose can significantly impact the after-tax returns of your GIC investment.

What Are the Drawbacks of GICs?

While GICs offer significant advantages, they also come with certain limitations that investors should consider before making a commitment.

- Lower returns: GICs’ principal guarantee and predictability come at the cost of typically lower returns compared to equity investments.

- Inflation risk: GICs face the risk that their returns may not keep pace with inflation, potentially eroding the purchasing power of your investment.

- Opportunity costs: Committing funds to GICs may prevent you from taking advantage of potentially higher returns available through other investments.

- Tax considerations for Non-Registered Accounts: Interest earned on non-registered GICs is fully taxable as income at your marginal tax rate, which is typically higher than the preferential tax treatment given to capital gains or dividends.

How to Invest in a GIC?

Before purchasing a GIC, you’ll need to establish an appropriate account. This typically requires:

- Valid government-issued photo identification

- Social Insurance Number (SIN)

- Proof of address (utility bill, bank statement, etc.)

- Banking information for fund transfers

- Completed application forms (varies by institution)

If you’re purchasing the GIC within a registered account (TFSA, RRSP, FHSA, LIRA), you’ll need to open or have that account structure in place first.

The GIC purchase process typically follows these steps:

- Research and comparison: Shop around for competitive rates and terms

- Select GIC type and term: Choose the specific GIC that meets your needs

- Complete application: Fill out required forms (online or in person)

- Fund the investment: Transfer money from your account to purchase the GIC

- Receive confirmation: Get documentation confirming your GIC purchase

- Track maturity date: Mark when your GIC will mature for reinvestment planning

Many financial institutions across Canada now offer online GIC purchases, streamlining this process significantly, such as:

- Banks: Major banks like RBC, TD, Scotiabank, BMO, and CIBC offer extensive GIC products

- Credit Unions: Often provide competitive rates and additional features

- Trust Companies: Specialized financial institutions with GIC offerings

- Online Banks: Digital banks like Tangerine, EQ Bank, and Simplii Financial frequently offer higher rates

- Brokerages: Investment dealers can provide access to GICs from multiple institutions

Each provider type has advantages regarding rates, features, and accessibility. Online banks typically offer higher rates due to lower overhead costs, while traditional banks may provide more personalized service and broader product options.

How to Choose the Right GIC for Your Needs?

Selecting the right GIC requires careful consideration of your financial situation, goals, and market conditions. Follow these steps to make an informed decision.

- Assessing your financial goals: Begin by clearly defining what you’re trying to achieve with your GIC investment. Your goals will dictate the type of GIC, term length, and account structure most appropriate for your situation.

- Determining your time horizon: Your investment time horizon, or how long you can keep your money invested, is crucial in selecting the right GIC. Matching your GIC term to your time horizon helps optimize returns while ensuring funds are available when needed.

- Evaluating your risk tolerance: While GICs are generally low-risk investments, different types carry varying degrees of risk. Your comfort with these different risk levels should influence your GIC selection.

- Comparing GIC rates between institutions: GIC rates can vary significantly between financial institutions, sometimes by more than 1% for identical terms. Shop around to find the best rates.

- Considering tax implications: The tax treatment of your GIC interest can significantly impact your after-tax returns. Your current and expected future tax brackets should influence these decisions.

FAQs About Guaranteed Investment Certificates GICs

Why do longer-term GICs pay higher interest rates?

Longer-term GICs generally offer higher interest rates to compensate investors for the increased risk and reduced flexibility associated with committing their money for extended periods. These risks include inflation risk (the potential decrease in purchasing power over time), opportunity cost (missing out on potentially better investments), and interest rate risk (being locked into a rate if market rates increase).

Where can I find the best GIC rates in Canada?

The best GIC rates are typically found at online banks, credit unions, and smaller financial institutions rather than the major banks. Online rate comparison websites like Ratehub.ca, RATESDOTCA, and Finder.ca provide up-to-date comparisons across numerous institutions. Credit unions often offer competitive rates to attract deposits, while online banks have lower overhead costs, allowing them to offer higher rates.

Can I include GICs in my RRIF?

Yes, GICs can be held within a Registered Retirement Income Fund (RRIF) and are a popular choice for retirees seeking stable, predictable income. RRIF GICs provide the same principal protection and guaranteed returns as other GICs while helping satisfy mandatory RRIF withdrawal requirements. The interest earned remains tax-sheltered until withdrawal.

Are GICs a Good Investment?

GICs are excellent investments for specific purposes, particularly for investors seeking safety, predictability, and capital preservation. They're well-suited for: Emergency funds requiring principal protection, Saving for specific short to medium-term goals, Conservative portions of investment portfolios, and Risk reduction as retirement approaches. However, GICs may not be ideal for long-term growth objectives or beating inflation over extended periods. Their appropriateness depends on your financial goals, time horizon, and risk tolerance.

What tax documents will I receive for my GIC investments?

Non-registered GICs typically receive a T5 Statement of Investment Income (or Relevé 3 in Quebec) reporting interest income earned during the tax year. For GICs that compound interest until maturity, you may receive T5 slips annually reporting the accrued interest, even though you haven't received the payment yet. For registered account GICs (TFSA, RRSP, FHSA), no tax slips are issued for the interest earned while funds remain in the registered account.

Summary

Guaranteed Investment Certificate GIC represents a cornerstone of safe investing in Canada, offering predictability and security that few other investments can match. While they may not offer the highest potential returns compared to market-based investments, GICs fulfill specific and important roles within a comprehensive financial plan.

Whether you’re saving for a home, building an emergency fund, or creating a stable income for retirement, GICs deserve consideration as part of your financial toolkit. Their combination of safety, predictability, and guaranteed returns addresses critical needs that more volatile investments simply cannot fulfill.