Planning a trip, whether abroad or within Canada, involves more than just booking flights and hotels. A good travel insurance plan can protect travellers from unexpected medical expenses, trip cancellations, and lost baggage that could otherwise cost thousands of dollars.

Lifebuzz makes it easy to compare coverage options, understand costs, and find the policy that best suits your needs.

What Is Travel Insurance?

Travel insurance is a type of insurance that protects you against unexpected costs that arise during your trip, whether you’re travelling within Canada, abroad, or visiting Canada from another country.

Travel insurance has two main categories: travel medical coverage and trip protection. Emergency medical insurance covers unexpected medical expenses during your trip, including hospitalization and repatriation in case of death. Trip protection insurance reimburses non-refundable costs if you must cancel before departure or return home early.

The value of travel insurance goes beyond financial coverage. It provides 24/7 emergency assistance, access to any trusted hospitals worldwide, and peace of mind knowing that an unexpected health issue won’t derail your trip.

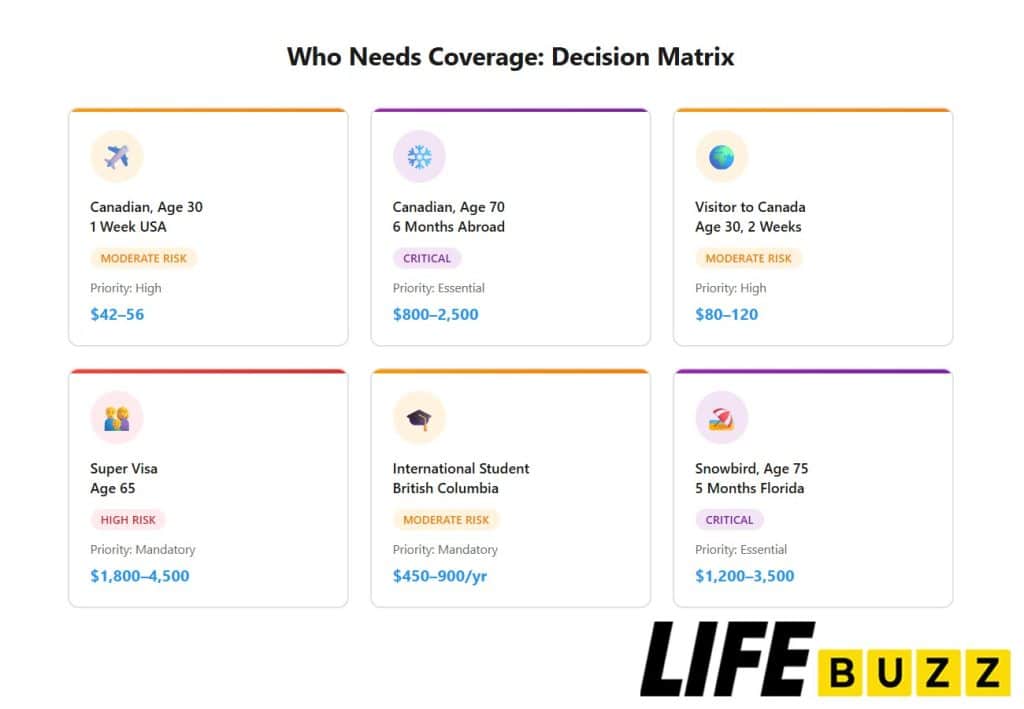

Who Needs Travel Insurance

Provincial health plans provide very limited coverage for medical care outside Canada, and Canada’s healthcare system also doesn’t cover visitors. This creates two distinct groups who need travel insurance: Canadians travelling abroad and visitors coming to Canada.

Canadians Travelling Abroad

Every Canadian travelling internationally needs emergency medical travel insurance, regardless of trip duration or destination, as provincial health coverage ends the moment you cross the border. Ontario’s OHIP pays a maximum $400 per day for hospital stays outside Canada, while a U.S. hospital charges $3,000 to $10,000 per day, leaving you to pay thousands of dollars out of pocket.

Even travel within Canada can expose you to coverage gaps. Provincial reciprocal agreements cover emergency care in other provinces but exclude ambulance services (ranging from $500 to $2,000 per trip), prescription drugs (only when hospitalized), private hospital rooms, and emergency dental services. A broken leg in British Columbia costs an Ontario resident $1,500 to $3,000 in uncovered ambulance and follow-up care expenses.

Purchasing travel insurance fills the gaps, whether you’re travelling abroad or between provinces.

Visitors to Canada

Similarly, visitors to Canada, including tourists, international students, temporary workers, and family members staying on a Super Visa, are not covered by the provincial healthcare system.

Without insurance, even a minor accident or illness can result in substantial costs. That’s why travel medical insurance is essential for anyone visiting Canada.

What Does Travel Insurance Cover?

When shopping for travel insurance, Canadians can choose from several types of coverage designed to meet different travel needs and budgets.

Emergency Medical Insurance

Emergency medical insurance is the most common type of travel insurance, providing coverage for unexpected medical expenses incurred while travelling. It covers hospitalization, physician fees, diagnostic tests like X-rays and MRIs, prescription medications, and ambulance services when you experience a medical emergency outside your home province.

Coverage limits typically range from $50,000 to $10 million, with higher limits recommended for destinations with expensive healthcare systems like the United States. When selecting an emergency medical policy, consider factors such as your age, health status, destination, and trip duration to ensure you have adequate coverage for your specific needs.

Trip Cancellation and Interruption Insurance

Trip cancellation and interruption insurance provides financial protection if you need to cancel your trip before departure or cut it short due to a covered reason, such as:

- Illness or injury (you, a travelling companion, or a family member)

- Death of a family member

- Severe weather or natural disaster

- Job loss

- Jury duty or court subpoena

Trip cancellation coverage reimburses you for prepaid, non-refundable trip expenses, such as flights, accommodations, and tours, if you need to cancel for a covered reason.

Trip interruption coverage, on the other hand, provides reimbursement for unused, non-refundable trip expenses and additional costs incurred if you need to return home early. It also covers the delay of flights by the airlines.

Baggage Insurance

Baggage insurance covers lost, stolen, damaged, or delayed luggage and personal belongings during travel.

Baggage loss, theft, or damage coverage applies when your belongings are permanently gone or destroyed. It reimburses you for the value of your items up to a specific limit.

Delayed baggage coverage activates when a carrier, such as an airline, temporarily loses your checked bags for a specified period, typically 6 to 12 hours. This benefit reimburses you up to a set limit for the purchase of essential items like toiletries, undergarments, and a change of clothes to tide you over.

All-Inclusive Travel Insurance

All-inclusive travel insurance combines multiple coverage types into a single, integrated package. A typical all-inclusive plan might include:

- Emergency medical coverage

- Trip cancellation and interruption coverage

- Baggage loss or delay coverage

- Flight accident coverage

- Travel accident coverage

The main advantage of all-inclusive insurance is the convenience and broad protection it provides. However, this plan is usually more expensive than standalone policies.

What Types of Travel Insurance Are Available in Canada?

As travel insurance needs vary based on who you are, where you are visiting, and the purpose of your trip, providers in Canada offer several types of plans tailored to each group.

Travel Insurance for Canadian Travellers

Canadians taking vacations, whether weekend getaways to nearby destinations or extended international adventures, represent the largest group of travel insurance purchasers. This insurance provides coverage for emergency medical care, medical evacuation, trip cancellation, and baggage protection while travelling abroad.

Snowbird Insurance

This is a specialized form of travel insurance for Canadians who escape winter by spending 2-8 months in warmer climates, typically Florida, Arizona, or Mexico. Snowbird insurance covers extended stays abroad, with most policies designed for trips lasting 4-8 months.

Provincial health coverage may end if the traveller exceeds 6 months on one trip. Most snowbird policies require you to maintain your provincial healthcare by returning to Canada between trips and staying within the maximum days allowed outside your province. Exceeding these limits can void both your travel insurance and provincial coverage.

Visitors to Canada Insurance

Visitors to Canada insurance covers emergency medical care for non-Canadians visiting Canada. Trip cancellation, baggage protection, and other non-medical benefits are not included.

Most plans allow travellers to travel to another country but must return to Canada by a specified time. However, medical expenses outside Canada are not covered.

Super Visa Insurance

Parents and grandparents of Canadian citizens and permanent residents are required to have Super Visa insurance to enter Canada. Legal requirements mandate a minimum $100,000 coverage for 365 days, paid in full upfront before visa approval.

Travel Insurance for International Students

International students studying in Canada typically require private medical insurance, either because provincial healthcare has waiting periods or because student-specific coverage offers more comprehensive benefits. Some provinces, like British Columbia, Alberta, and Saskatchewan, require students to purchase insurance during their first 90 days before provincial plans begin.

Travel Insurance for Foreign Workers

Foreign workers in Canada, whether on temporary or permanent work permits, face varying insurance requirements depending on their employer’s coverage and provincial waiting periods. Workers with employer-sponsored health benefits may not need additional insurance. Those without employer coverage must purchase private insurance during provincial waiting periods or indefinitely if their employer provides no benefits.

Which Travel Insurance Plan Fits You Best?

Once you’ve chosen the type of insurance that fits your situation, the next step is selecting a plan that matches your travel frequency and duration. Three common options are Single-trip, Multi-trip/Annual, and Top-up insurance.

Single-Trip Travel Insurance

Single-trip travel insurance is the most basic and common type of travel insurance, best for occasional vacations. It provides coverage for a single trip with a specified start and end date.

Coverage limits and benefit amounts can vary widely between providers and policies, so it’s important to compare your options and choose a plan that meets your specific needs.

Multi-Trip or Annual Travel Insurance

Multi-trip annual plans work best for frequent travellers, business travellers, and anyone taking three or more trips per year. Rather than purchasing separate single-trip policies for each trip, this plan provides coverage for an unlimited number of trips within a 12-month period.

You cannot exceed the per-trip maximum. If you purchase an annual plan with a 10-day limit, each trip must be 10 days or less in duration. Trips exceeding the annual plan days can purchase top-up insurance for that one trip. Most insurers allow you to upgrade mid-year by paying the difference.

How Top-up or Extension Coverage Works

Top-up insurance will add additional coverage to your existing travel insurance plan. It is usually used when your annual plan is insufficient. You must purchase top-ups before your current policy expires. Most insurers require a 24 to 72-hour notice; you cannot buy top-ups after coverage lapses or while hospitalized with an active claim.

On a trip that is being extended, the current policy just needs to be extended. The terms, conditions, coverage amounts, and deductibles of your original policy remain exactly the same. New coverage becomes effective when the extension is paid. Some insurers offer small discounts when extending existing policies.

The following table summarizes common eligibility scenarios for extending coverage:

| Scenario | Extension Allowed? | Requirements |

|---|---|---|

| Healthy, decide to stay longer, 3 days before expiry | Yes | Purchase before the current policy ends |

| Developed flu, want to extend | No | Medical instability excludes top-up |

| Currently hospitalized | No | Active claim voids top-up eligibility |

| Healthy, policy expired yesterday | No | Must purchase before expiry |

| Healthy, 1 week before expiry | Yes | Standard top-up process |

How Much Does Travel Insurance Cost in Canada?

Travel insurance typically costs 4-10% of total trip cost for all-inclusive coverage, with medical-only plans as low as 1-2% for young, healthy travellers. The following examples illustrate typical travel insurance costs in 2025:

| Age | Traveller Type | 7-Day Trip | 30-Day Trip | Annual Multi-Trip (10 days) |

|---|---|---|---|---|

| 25 | Canadian to the USA | $35 – $55 | $75 – $110 | $180 – $260 |

| 25 | Visitor to Canada | $45 – $65 | $95 – $140 | $450 – $650 |

| 45 | Canadian to the USA | $60 – $95 | $140 – $210 | $320 – $480 |

| 45 | Visitor to Canada | $85 – $125 | $220 – $340 | $1,100 – $1,700 |

| 65 | Canadian to the USA | $110 – $180 | $280 – $450 | $650 – $950 |

| 65 | Visitor to Canada (1 year) | Not applicable | Not applicable | $2,200 – $3,800 |

Actual premiums vary based on several factors, including your age, health status, trip duration, destination, coverage limits, and deductible selection.

- Age and health condition: Older travellers and those with pre-existing medical conditions generally face higher premiums.

- Trip length and destination: Longer trips and destinations with high healthcare costs (like the U.S.) will increase the price.

- Coverage limits: The more comprehensive the plan and the higher the coverage limits, the higher the cost.

- Deductible: Opting for a higher deductible (the amount you pay before insurance kicks in) can lower your premium.

Annual multi-trip insurance costs approximately twice the price of a single 10-day trip but covers unlimited trips throughout the year. If you travel 3+ times annually, annual coverage saves money. For comprehensive trip planning, budget 5-7% of the total trip cost for all-inclusive travel insurance.

Once you understand how pricing works, the next step is choosing a provider that offers reliable coverage at a fair rate.

Best Travel Insurance Providers in Canada

Canadian travellers can choose from numerous insurance providers, each offering different coverage limits, benefits, and pricing structures. Understanding how major providers compare helps you select the best option for your specific travel needs.

The table below provides a brief overview of leading insurance providers in Canada:

| Provider | Medical Coverage Limit | Trip Cancellation Limit |

|---|---|---|

| Manulife | $10 million | $5,000 |

| Blue Cross | $5 million | $1,500 to $5,000 |

| Allianz Global | $10 million | $1,500 |

| RBC Insurance | Unlimited | $1,500 |

| TD Insurance | $5 million | $1,500 |

| Scotia Insurance | $10 million | $3,500 |

| BMO Insurance | $5 million | $1,500 |

| CIBC Insurance | $10 million | $2,000 |

| Tugo | $10 million | $1,500 |

| GMS | $5 million | $5,000 |

| Travelance | $5 million | $2,500 |

Major Canadian banks, TD, RBC, BMO, CIBC, and Scotiabank, all offer travel insurance products. These bank-affiliated policies are often solid all-inclusive options for the average traveller with straightforward needs. If you already bank with these institutions, you can manage your insurance alongside other financial products. However, their claims processes can sometimes be less specialized than those of dedicated insurance companies.

Specialized providers that focus exclusively on insurance, like Blue Cross, Allianz, and GMS, are excellent choices for travellers with more complex needs. They offer more flexible and comprehensive policies and better claims support.

Consider your priorities when choosing between banks and specialized providers. For a detailed comparison of coverage, pricing, and reputation, check out our guide to the best providers for travel insurance in Canada.

How Pre-Existing Conditions Affect Travel Insurance Coverage

One of the most common concerns for travellers shopping for travel insurance is how pre-existing medical conditions can affect their coverage. Most travel insurance policies have a stability requirement for pre-existing medical conditions, which means your condition must be stable and controlled for a certain period of time (usually ranging from 7 to 180 days) before your coverage begins.

In general, a pre-existing medical condition is considered stable if:

- There have been no new symptoms, diagnoses, or treatments

- There have been no changes in medication or dosage

- There have been no hospitalizations or referrals to a specialist

- There have been no test results showing a deterioration of the condition

If your condition meets these criteria for the specified stability period, it will typically be covered under your travel insurance policy. However, if you have a medical emergency related to a pre-existing condition that was not stable, your claim may be denied.

Some providers offer policies specifically designed for travellers with pre-existing conditions, which may have more lenient stability requirements or cover certain unstable conditions for an additional premium.

Alternatively, you may be able to purchase a waiver or rider that lowers the stability days requirement, although this will likely come at a higher cost.

When to Purchase Your Travel Insurance Policy

Buy travel insurance as soon as you make your first trip payment or booking. Early purchase maximizes your trip cancellation coverage, protecting deposits and prepaid expenses from the moment you commit to your vacation. If you wait until closer to departure, you’ll have limited or no coverage for cancellations that occur before your policy purchase date.

Trip cancellation insurance typically requires purchase within 7-14 days of making your initial trip deposit to cover pre-existing medical conditions without additional exclusions. This “early purchase window” provides your broadest possible coverage. Missing this window doesn’t prevent you from buying insurance, but pre-existing conditions may be excluded even if they are stable.

Avoid purchasing insurance at the last minute. Buying coverage the day before departure limits your cancellation protection and may trigger additional medical screening requirements. Plan to secure your policy within one week of booking your trip for optimal coverage and pricing.

When Should You Consider Credit Card Travel Insurance?

Many premium credit cards include built-in travel insurance when you purchase the entire vacation using the card.

Coverage typically includes trip cancellation benefits ($1,500 to $5,000), baggage delay reimbursement ($100 to $500), rental car damage protection, and emergency medical coverage ranging from $500,000 to $1 million on high-end cards.

However, this coverage often comes with significant limitations. It applies only to people travelling by air and will not cover if the client is driving to their vacation.

Medical coverage caps of $500,000 to $1 million may fall short in destinations with expensive healthcare, and pre-existing medical conditions are typically not covered.

Trip booking requirements also mean that only the portions paid for with the card are eligible for reimbursement. Most policies limit coverage to trips lasting 15-21 days and may exclude travellers aged 65 and older or reduce benefits for older age groups.

Therefore, credit card insurance may be enough for short trips under 15 days, younger travellers (under 60) in good health, and journeys fully paid for with the card.

How to File a Travel Insurance Claim

Filing a travel insurance claim requires prompt communication with your insurer, careful documentation, and timely submission of all the necessary materials. Most insurance companies require you to report a claim within 48 hours after the first occurrence of insurance is used.

If a medical emergency occurs, contact your insurer immediately. They can arrange direct billing with hospitals, so you won’t need to pay up front.

If you must pay for medical care upfront, obtain receipts showing the date of service, services provided, diagnosis, healthcare provider’s name and credentials, and total amount charged. Most insurers require you to submit your claim within 30 to 90 days of treatment.

For trip cancellation or interruption claims, you’ll need to provide documentation, such as a medical certificate explaining why travel was not possible, original booking confirmations, cancellation receipts showing non-refundable costs, and proof of payment. Ensure your claim form is fully completed and all documents are attached; missing paperwork can delay processing by several weeks

Simple medical claims are typically processed within 2-4 weeks, while more complex cases that require medical review can take 1-3 months. Submitting a complete claim package the first time is the best way to avoid unnecessary delays.

Get the Cheapest Travel Insurance Quote in Canada

Saving money is great, but the ultimate goal is to find the best value: excellent coverage at a fair price. Here’s how to do it.

- Compare Quotes: Online tools are your best bet for quickly comparing quotes from multiple providers side by side. Enter your trip details once and see dozens of options.

- Bundle for Families and Groups: If you’re travelling with others, a family or group plan is often cheaper than buying individual policies.

- Don’t Pay for Unnecessary Coverage: Assess what you truly need. If your trip is fully refundable, you might not need high trip cancellation limits. If you have coverage through work benefits, check for overlaps.

- Consider Your Deductible: A policy with a zero deductible will cost more. By choosing a higher deductible, you agree to cover that initial amount yourself in case of a claim, which lowers your premium. Just be sure you can comfortably afford the deductible you choose.

- Buy Early: Purchase your insurance as soon as you book your trip to ensure that trip cancellation benefits immediately cover you.

With a little research and smart planning, you can find affordable travel insurance that keeps you protected wherever your trip takes you.

FAQs about Travel Insurance in Canada

What’s the difference between trip cancellation and interruption?

Trip cancellation insurance reimburses prepaid, non-refundable expenses when you must cancel your trip before departure. Trip interruption insurance covers costs when you need to cut your trip short after departure or covers unused portions and additional transportation to return home. The key difference is timing; cancellation applies before you leave, and interruption applies after your trip begins.

Do I need travel insurance within Canada?

Yes, travel insurance provides valuable protection even for interprovincial trips within Canada. Your provincial health plan offers limited coverage in other provinces and doesn’t cover ambulance services, prescription drugs, private hospital rooms, and other related expenses.

Can I buy travel insurance after leaving Canada?

Yes, but with significant limitations. Most Canadian insurers allow post-departure purchases; however, policies include 48-hour waiting periods during which illness or injury is not covered.

Pre-existing conditions are typically excluded entirely from post-departure policies. Trip cancellation coverage isn’t available after departure since you’ve already left.

The best practice is to always purchase before departing to receive full protection from day one.

What doesn’t travel insurance cover?

Common exclusions across most policies include:

– Non-emergency medical care (routine checkups, elective procedures)

– Pre-existing conditions, unless stable and disclosed

– High-risk activities without specialized add-on coverage

– Alcohol or drug-related incidents

– Travel to destinations under government advisories

– Mental health emergencies (some policies)

– Pregnancy complications after week 32

– Cancellations for non-covered reasons (changed your mind, fear of flying) and illegal activities

Always read your specific policy’s exclusion list carefully before purchasing; exclusions vary by insurer and policy type.

What’s the difference between single-trip and annual travel insurance?

Single-trip insurance covers one specific journey from start to end date, ranging from 1 to 365 days. This suits travellers taking 1-2 trips annually. Annual multi-trip insurance covers unlimited trips within 365 days, with each trip capped at a selected maximum (typically 4, 10, 18, 30, or 60 days). Frequent travellers, business travellers, and anyone taking 3+ trips annually save money with annual plans. You must return to your province between trips to reset the counter.

Can I get a refund on my travel insurance?

Yes, in most cases. Full refunds apply if you cancel before your trip’s departure date and haven’t filed any claims.

Some policies allow pro-rated refunds for unused portions of coverage when cancelling long-term policies mid-term.

Annual multi-trip policies may offer partial refunds if cancelled mid-year without claims. Check your specific policy’s cancellation terms before purchasing; policies vary significantly.

The Bottom Line

Travelling should be about creating incredible memories, not worrying about what could go wrong. Investing in the right travel insurance is one of the smartest decisions you can make. It protects your health, your finances, and your peace of mind. Take the time to compare your options, read the policy details carefully, and select a plan that suits your unique needs.