What would happen if a medical emergency struck during your Canadian vacation? While Canada is celebrated for its universal healthcare system, this coverage is reserved for residents, leaving visitors financially vulnerable to unexpected medical emergencies.

This is where travel insurance for visitors to Canada becomes an essential safeguard. We will explore what visitor insurance is, what it covers, how much it costs, and how to choose the perfect plan for your trip, ensuring you can enjoy your Canadian journey with complete peace of mind.

What Is Visitor to Canada (VTC) Insurance?

Visitor to Canada insurance is a private health insurance plan that protects non-residents travelling in Canada from the high costs of medical care. Unlike travel trip insurance that covers cancellations and lost baggage, this is emergency medical coverage designed specifically for the Canadian healthcare system.

Do you really need travel insurance to visit Canada? Imagine a parent visiting their family in Vancouver experiences sudden chest pains. They require an ambulance, an emergency room visit, diagnostic tests, and a two-day hospital stay. Without coverage, the bill could easily exceed $15,000. A proper travel insurance shields them from staggeringly high out-of-pocket medical expenses.

Who Needs Visitors to Canada Insurance?

Travel insurance is NOT mandatory for visitors to Canada, except for specific visa categories. However, the Government of Canada and Immigration, Refugees and Citizenship Canada (IRCC) strongly recommend that all visitors obtain emergency medical coverage before arrival.

Tourists and temporary visitors visiting Canada for vacation, business, or to see family should have coverage for their entire stay to prevent financial risks. Canadian citizens who have lived abroad for more than six months may lose their provincial coverage and will need temporary private insurance when they return. International students and foreign workers who face a waiting period before qualifying for provincial health insurance plans also need this visitor insurance to bridge the gap.

The only visitors legally required to purchase insurance are Super Visa applicants applying for extended stay visas. Without proof of this coverage, IRCC will deny the Super Visa application.

Visitor Insurance for Super Visa Applicants

The Super Visa program is a popular pathway offered by IRCC that allows parents and grandparents of Canadian citizens and permanent residents to visit for extended periods. A non-negotiable requirement of this program is that all applicants must provide proof of private medical insurance from a Canadian company. This mandatory policy is known as Super Visa insurance.

To be valid, a Super Visa insurance policy must meet strict criteria set by Immigration, Refugees and Citizenship Canada (IRCC): coverage must total at least $100,000 CAD, remain valid for at least one year from the visa holder’s arrival date, cover emergency medical care, hospitalization, and repatriation, stay active each time the visa holder enters Canada, and originate from a Canadian insurance company.

Given the age demographic and coverage requirements, Super Visa insurance typically costs more than standard visitor policies. However, this mandatory protection ensures parents and grandparents receive necessary care during extended family visits without placing financial burdens on their Canadian relatives.

Visitor Insurance for International Students

For the thousands of international students who choose Canada for their education, private health insurance is not just a recommendation; it’s a necessity. This is because most provinces, including Ontario, British Columbia, and Quebec, impose a waiting period of up to three months before a student is eligible for their provincial health insurance plan.

Many providers in Canada offer coverage of up to $2 million for student insurance, typically including all standard emergency medical coverage. Some policies even include benefits tailored to students, such as mental health support or coverage for tutorial services in the event of a medical emergency that interrupts their studies.

Students should purchase coverage before departing their home country to avoid waiting periods that most insurers impose when purchasing after arrival in Canada. Comparing quotes from multiple providers ensures students find appropriate coverage at competitive rates while meeting any requirements their educational institution may have for proof of insurance.

Visitor Insurance for Foreign Workers

Similarly, foreign workers on work permits face waiting periods before qualifying for provincial health insurance plans. During this time, they are uninsured for healthcare. A temporary policy bridges this gap, protecting them from potentially high costs for emergency medical expenses.

Workers in their 30s generally pay toward the lower end of this range, while those in their 50s pay higher premiums reflecting increased health risks.

Visitor Insurance for Returning Canadians

When Canadians return home after extended international work assignments, education abroad, or retirement elsewhere, they must serve a new waiting period, typically three months in Ontario, British Columbia, and Quebec, before provincial coverage is reinstated.

A short-term visitor policy is the only way to protect against medical costs during this uninsured period. This also applies to Canadians moving between certain provinces who may face a temporary lapse in their provincial health insurance plan.

Similarly, Canadians moving from one province to another may experience temporary coverage gaps while establishing residency in the new province. Consequently, visitor insurance serves as a practical solution for protecting health and finances during interprovincial relocations as well as international returns.

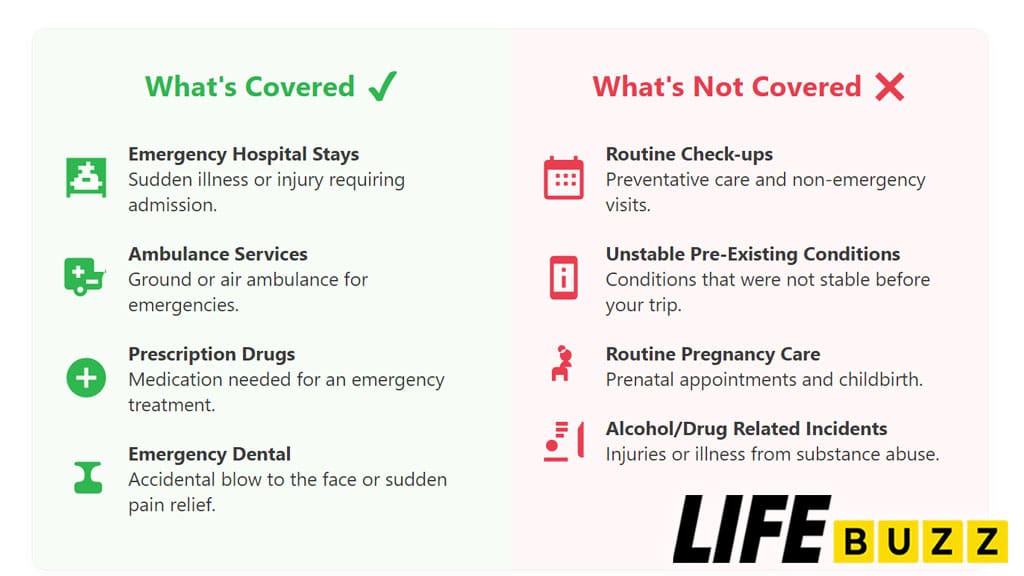

What Does Visitor to Canada Insurance Cover?

Beyond just covering a hospital bill, what specific protections can you expect from a standard policy? A comprehensive visitor insurance plan is designed to cover a wide array of emergency-related expenses.

- Emergency Medical Expenses: This is the cornerstone of the policy, covering costs for treatment of sudden illnesses or injuries. This includes physicians’ fees, diagnostic tests like X-rays and bloodwork, and hospital room charges.

- Hospitalization: Covers semi-private or private hospital accommodation, allowing for a more comfortable recovery.

- Prescription Drugs: Reimburses the cost of medications prescribed by a doctor to treat a covered medical emergency, typically for a 30-day supply.

- Emergency Medical Evacuation: Covers the cost of transportation to the nearest appropriate medical facility or, if medically necessary, transportation back to your home country. This is a critical benefit, as medical airlifts can cost tens of thousands of dollars.

- Repatriation: In the event of a death, this covers the significant costs associated with preparing and returning the deceased’s remains to their home country, up to a specified limit (e.g., $10,000).

- Emergency Dental: Provides coverage for accidental blows to the face requiring immediate dental work or for sudden dental pain relief, usually up to a smaller limit (e.g., $500 – $4,000).

- Paramedical Services: Includes the services of licensed professionals such as physiotherapists, chiropractors, or podiatrists when prescribed by a physician as part of emergency treatment.

- Accidental Death and Dismemberment (AD&D): This provides a lump-sum payment to the insured or their beneficiaries in the event of death or severe injury (such as loss of a limb) resulting directly from an accident.

What’s Not Covered: Common Exclusions

While Visitors to Canada insurance provides comprehensive protection for emergencies, it is not a blank cheque for all medical needs. Every policy contains a list of exclusions and limitations for which the insurer will not provide coverage.

- Unstable Pre-existing Conditions: Any condition for which you received treatment, had a change in medication, or had new symptoms in the 90-180 days before your trip.

- Non-Emergency & Elective Care: Routine check-ups, cosmetic procedures, or any treatment that can safely wait until you return home.

- General Pregnancy/Childbirth: Routine prenatal care and delivery. Some policies may cover complications of pregnancy if the pregnancy began after the policy was purchased and the trip is taken before a certain week (e.g., 31st week).

- Mental Health Conditions: Ongoing psychiatric care, therapy for anxiety or depression.

- Incidents Under the Influence: Injuries or illnesses resulting from the abuse of alcohol or non-prescribed drugs.

- High-Risk Activities: Extreme sports like mountaineering, skydiving, or racing, unless you purchase a specific “sports rider.”

For example, a tourist who comes to Canada with an unstable heart condition and experiences a complication related to that known issue may find their claim denied if their policy excludes unstable pre-existing conditions. Similarly, a student who decides to go skydiving without purchasing an optional adventure sports rider would not be covered for injuries sustained during that high-risk activity. Understanding these exclusions is vital to avoiding claim denials. Always read your policy document carefully.

Choosing the Right Type of Visitor Insurance Plan

Not all visitors have the same itinerary or needs, and fortunately, the insurance market offers a variety of plans to match. Selecting the right type of plan is crucial for ensuring you have appropriate and cost-effective coverage.

The best plan for you depends on your traveller profile. Are you a tourist, a frequent business traveller, an international student, or a parent on a Super Visa? For example, a student studying in Canada for a year has very different needs than a tourist visiting Niagara Falls for a weekend.

To help you decide, here are the most common types of visitor insurance plans and who they are designed for.

Single-Trip Plans

This is the most common type of policy. It provides coverage for one specific trip with defined start and end dates.

- Who it’s for: Tourists, families on vacation, or anyone making a one-time visit to Canada.

Multi-Trip Annual Plans

These plans cover multiple trips to Canada (and often other countries) within a 365-day period. Each individual trip has a maximum duration, such as 15 or 30 days.

- Who it’s for: Frequent business travellers, or individuals who live near the border and cross into Canada regularly.

How Much Does Visitor Insurance for Canada Cost?

The cost of visitor to Canada insurance is not one-size-fits-all; it is calculated based on a unique risk profile for each traveller. The core principle is simple: the higher the potential risk for the insurer, the higher the premium.

Key Factors Influencing Cost:

- Age of the Traveller: This is the most significant factor. Premiums increase substantially for older travellers, especially those over 65.

- Duration of Stay: Longer trips mean more time for a potential incident to occur, leading to higher costs.

- Coverage Amount: Policies with higher maximum limits cost more.

- Deductible: Choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) will lower your premium.

- Pre-existing Medical Conditions: Opting for a plan that covers stable pre-existing conditions will increase the premium.

For example, an 80-year-old visitor staying for six months with a pre-existing medical condition represents a higher risk than a healthy 25-year-old visiting for one week, so their premium will be significantly higher.

How to Compare and Purchase Visitor Insurance for Canada

The process of buying visitor insurance is straightforward and can be completed online in just a few minutes.

The best approach is to use an online comparison tool. This allows you to view quotes from multiple reputable insurers side-by-side, making it easy to find the best balance of coverage and cost. For instance, a user can enter their trip details once and instantly see offers from Manulife, TuGo, and Allianz, comparing their premiums, deductibles, and benefit limits.

Follow this simple, four-step process to get covered:

Step 1: Gather Your Trip and Traveller Details

You will need the traveller’s name, date of birth, country of origin, and their exact arrival and departure dates in Canada. You will also need to decide on the coverage amount (e.g., $100,000 CAD) and deductible.

Step 2: Compare Quotes from Top Providers

Use an online insurance brokerage or comparison website. Enter your details to generate a list of quotes. Pay close attention not just to the price, but to the coverage details, especially regarding any pre-existing medical conditions.

Step 3: Choose Your Policy and Review the Details

Once you’ve selected a plan, carefully read the policy wording before you buy. Understand the definitions, benefits, and exclusions. Ensure it meets all your needs, especially if you are applying for a Super Visa.

Step 4: Get Covered and Carry Your Documents

Complete the purchase online with a credit card. You will receive your policy documents and confirmation of coverage via email almost instantly. Be sure to print a copy and carry it with you during your travels in Canada.

Following these steps ensures you get the right policy for your needs, providing the necessary protection for your visit.

FAQs About Travel Insurance for Visitors to Canada

Here are answers to some of the most common questions travellers have about insurance for visitors to Canada.

Does visitor insurance cover pre-existing conditions?

Yes, many companies offer plans that cover stable pre-existing conditions. A condition is generally considered stable if there have been no changes in medication, treatment, or symptoms for a specific period (e.g., 90-180 days) before your trip.

Which company is the best for visitor insurance in Canada?

There is no single “best” company for everyone. The best provider for you depends on your age, health, trip duration, and budget. Companies like Manulife, GMS, TuGo, Allianz, Sun Life, and Travelance are all reputable providers in Canada. The most effective strategy is to use an online comparison tool to compare quotes and policy features from multiple insurers to find the one that offers the best value for your specific situation.

Can I extend my policy if my trip is longer than planned?

Yes, most policies can be extended. You must request the extension before your current policy expires, have not filed any claims, and have no change in your health status.

Is visitor insurance refundable?

Refunds are possible under certain conditions. You can typically get a full refund if you cancel before your effective date or during the 10-day “free look” period. Partial refunds may be available if you return to your home country early, provided you have not made any claims.

Do these policies cover side trips to other countries?

Most policies allow for short side trips (e.g., to the USA), as long as the majority of your trip is spent in Canada and your trip originates and terminates in Canada. Coverage may be limited to a certain number of days (e.g., 30 days).

The Bottom Line

Travelling to Canada should be an exciting experience, not a source of financial anxiety. While the country’s landscapes are welcoming, its healthcare system is not designed for visitors, and the out-of-pocket costs for a medical emergency can be overwhelming. Securing visitor to Canada insurance is the single most important step you can take to protect yourself and your loved ones.