For many Canadians, insurance is about preparing for the unexpected. Accidental Death and Dismemberment (AD&D) insurance is designed for exactly that, offering financial protection in the event of a serious accident that results in death, the loss of a limb, or the loss of a critical function like sight or hearing.

But is it a necessary purchase? How does it differ from traditional life insurance? This guide will explore what exactly AD&D insurance covers, who benefits from it, and how to decide if it’s the right choice for your financial plan.

What is AD&D surance?

Accidental Death and Dismemberment (AD&D) insurance is a type of policy that pays a benefit only if you die or suffer a severe, life-altering injury as a direct result of an accident. Unlike standard life insurance, which covers almost any cause of death, AD&D is limited exclusively to accidents. This narrow focus is what makes it significantly more affordable.

The policy pays out in two primary scenarios:

- Accidental Death: If you die from a covered accident, your beneficiaries receive the full policy amount, known as the death benefit.

- Dismemberment: If you survive an accident but lose a limb, your sight, your hearing, or your speech, the policy pays out a percentage of the benefit directly to you. This is often called a living benefit.

You can purchase as a standalone policy, through a group plan at work, or as an add-on (rider) to an existing life insurance policy.

What Does AD&D Insurance Cover?

AD&D insurance covers both accidental death and dismemberment/loss of critical functions in the event of an accident.

Fatal Accidents Covered

For a death benefit to be paid, the death must be a direct result of an accident and occur within a specific timeframe, often 90 days, as stipulated in the policy. Covered accidents generally include:

- Motor vehicle collisions, including car, motorcycle, bus, or pedestrian accidents. Latest data from Transport Canada shows that there were 1,964 motor vehicle fatalities in Canada in 2023, highlighting the risk of such incidents.

- Workplace accidents like falls, equipment malfunctions, electrocutions, and injuries involving machinery

- Drowning, fires, and exposure to the elements

- Falls from heights

- Natural disasters such as tornadoes, floods, or earthquakes

- Airplane, helicopter, or hot air balloon crashes

- Recreational accidents like boating, biking, horseback riding, or skiing

- Accidents involving firearms, explosives, or electrocution

Essentially, AD&D insurance covers deaths that occur due to violent external causes and not due to medical issues or natural causes. Death must occur within a specified timeframe of the accident for the benefit to be payable, usually within 90 days, depending on the policy.

Dismemberment and Loss of Function Covered

If an accident results in a specified injury but not death, the policy pays a portion of the benefit amount, known as a “living benefit”. This includes the loss of:

- Limbs such as arms, legs, hands, feet, fingers, or toes

- Sight in one or both eyes

- Speech

- Hearing in one or both ears

The policy contains a “schedule of losses” that outlines the percentage of the total benefit paid for each specific injury. For example, a typical schedule might look like this:

- Losing both arms may pay 100% of the death benefit

- Losing one arm may pay 50% of the death benefit

- Losing a finger may pay 5-10% of the death benefit

- Loss of sight in both eyes may pay 100% of the death benefit

- Loss of sight in one eye may pay 50% of the death benefit

- Complete loss of hearing may pay 50-100% of the death benefit

- Loss of speech may pay 50% of the death benefit

Note: These percentages are for illustrative purposes only and vary significantly between insurance providers. Always read the policy’s specific schedule of losses.

You may also want to know: Laser Eye Surgery Cost in Canada

What is Not Covered by AD&D Insurance?

While AD&D insurance covers a wide range of accidental injuries and deaths, most policies typically exclude certain circumstances, including the death or injury due to:

- Natural causes: Illness, disease, heart attacks, strokes, or infections.

- Suicide or intentionally self-inflicted injuries.

- War or acts of terrorism.

- Use of illegal drugs or impairment by alcohol (often including prescription drug misuse).

- Committing a criminal act.

- High-risk hobbies: Many policies exclude activities like scuba diving, auto racing, or hang gliding unless an additional premium is paid.

- Aviation: Accidents in private planes are often excluded, though travel as a fare-paying passenger on a commercial flight is typically covered.

Check your plan’s exclusions section carefully, as benefits will not be paid if death or dismemberment occurs due to excluded causes.

Who Needs AD&D Insurance?

AD&D insurance is designed to provide supplemental coverage and is especially beneficial for:

Individuals in High-Risk Occupations

According to the Association of Workers’ Compensation Boards of Canada (AWCBC), there were 993 workplace fatalities recorded in Canada in 2022. Industries like construction, transportation, manufacturing, and mining carry a higher risk of serious accidents, making AD&D a valuable layer of protection.

Younger Individuals

Accidents are consistently among the leading causes of death in Canada. For people under 45, accidents are a leading cause of death in Canada. An AD&D policy can provide affordable financial protection for a young family that might not yet be able to afford a large traditional life insurance policy.

Premiums are lowest when purchasing at younger ages under 40. Those with young families can benefit from AD&D policies to protect loved ones.

Those Seeking to Supplement Existing Insurance

Many people purchase AD&D coverage in addition to their regular life insurance policy. This provides extra coverage specifically for accidental death, essentially “doubling” the death benefit if you pass away due to an accident.

Individual with Limited Budgets

Because of its limited nature, AD&D is a budget-friendly way to secure some level of financial protection against unforeseen events. This makes it viable for middle-income families or individuals who want supplemental protection without high costs.

How Much Does AD&D Insurance Cost?

There are five main factors that impact the cost of AD&D insurance:

- Age: Premiums increase as you get older

- Amount of coverage: More coverage means higher premiums

- Type of policy: Group policies are cheaper than individual policies

- Insurer: Rates can vary significantly by insurance provider

- Extra benefits: Policies with additional features may cost more

AD&D insurance is relatively inexpensive compared to regular life insurance because policies pay out only for accidents. Here is a sample quote for AD&D products from Sun Life:

- Family: $0.6 per $10,000 of death benefit per month

- Individual plans: $0.39 per $10,000 of death benefit per month

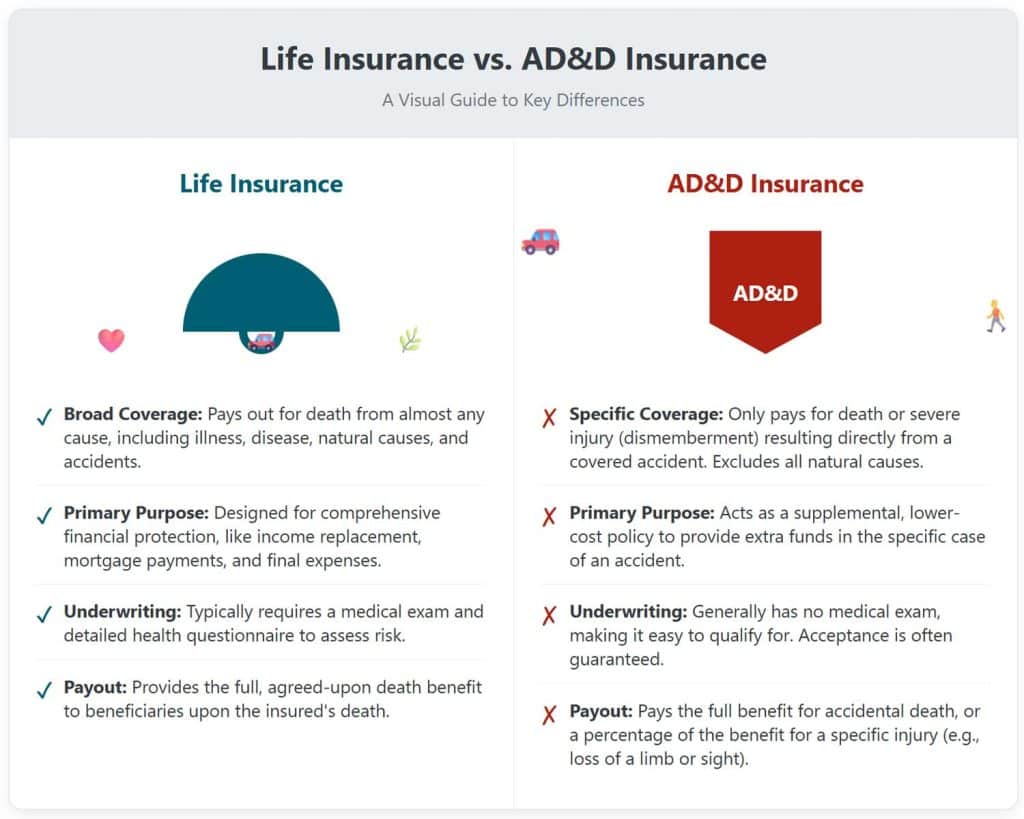

AD&D vs. Traditional Life Insurance: What’s the Difference?

This is the most critical distinction to understand. While both offer financial protection, they serve very different purposes.

| Feature | Accidental Death & Dismemberment (AD&D) | Standard Life Insurance |

|---|---|---|

| Coverage Scope | Covers only death or injury from an accident. | Covers death from nearly any cause, including illness (e.g., cancer, heart attack) and natural causes. |

| Payout Conditions | Pays a full benefit for accidental death and a partial benefit for specific injuries (dismemberment). | Pays the full death benefit only upon death. Does not cover injury. |

| Underwriting | Usually requires no medical exam. Acceptance is almost guaranteed. | Typically requires a medical exam and a detailed health questionnaire. |

| Cost | Very affordable due to its limited coverage. | More expensive because the risk of a payout is much higher for the insurer. |

| Best For… | Supplementing existing insurance, those in high-risk jobs, or individuals who can’t qualify for traditional life insurance due to health issues. | Acting as the primary foundation of financial protection for your family. |

Note: Do not treat AD&D insurance as a replacement for traditional life insurance. The majority of deaths are due to illness, which AD&D does not cover. Think of AD&D as a specific supplement, not a primary safety net.

Where Can You Purchase AD&D Insurance?

There are three ways to get AD&D insurance coverage in Canada:

As a Rider on Your Existing Life Insurance Policy

Most insurers allow you to add an AD&D rider to your term or permanent policy. This supplements the regular death benefit with extra accidental death coverage for a small additional premium. This is the easiest way to obtain it if you already have life insurance.

Via Employer or Group Plan

Many companies offer AD&D as part of their employee benefits package. This is usually the most affordable and convenient option, with premiums paid through payroll deductions.

As a Standalone Policy from an Insurer

You can buy individual AD&D policies as standalone coverage directly through major insurance companies like Sun Life, Canada Life, RBC Insurance, BMO Insurance, and more. Premiums are higher than group plans, but may be more cost-effective for large amounts of coverage.

The AD&D Claims Process

If you or a beneficiary needs to file a claim, the process generally involves these steps:

- Notify the Insurer or Plan Sponsor: Contact the insurance company or your employer’s benefits administrator as soon as possible.

- Complete the Claim Forms: You will need to fill out detailed forms. For a death claim, the beneficiary will complete them; for a dismemberment claim, the insured person will. These forms often require an employer’s statement if it is a group plan.

- Provide Supporting Documentation: This will include a physician’s statement, an accident report, and, in the case of death, a death certificate. Be thorough and provide as much detail as possible.

- Claim Review: The insurer will review the submitted information against the policy’s terms. They may request additional information. According to Canada Life, a decision is typically made within 7 days of receiving all necessary documents, though complex cases can take longer.

What to Do If Your Claim is Denied

Insurers may deny claims for various reasons, such as a belief that the death was not accidental, the injury does not meet the policy definition, or an exclusion applies. If your claim is denied:

- Review the Denial Letter: The insurer must provide a written explanation for their decision.

- File an Internal Appeal: All insurers have a formal appeal process. Your denial letter should outline the steps to appeal the decision.

- Seek Independent Assistance: If your appeal is unsuccessful, you can turn to the OmbudService for Life & Health Insurance (OLHI). OLHI is a free, impartial national service that helps consumers resolve disputes with their insurance providers.

How to Choose the Right AD&D Policy

When comparing AD&D policies or riders, look beyond the premium and coverage amount. Here’s how to make a smart decision.

Assess Your True Need vs. Want

First, be honest about your risk. Do you work in a dangerous job or have a long commute? If so, your risk of an accident is higher. Then, look at your existing life insurance. Is it sufficient to cover your family’s needs? AD&D should fill a specific gap, not just be an impulse buy.

Compare AD&D vs. More Life Insurance

This is the key calculation. Get a quote for the AD&D policy you’re considering. Then, ask your life insurance provider how much your premium would increase to add the same amount of coverage to your existing term policy.

Read The Policy Wording Carefully

If you decide AD&D is right for you, read the fine print carefully.

- Definition of “Accident”: Ensure it’s broad and doesn’t have unreasonable limitations.

- Schedule of Losses: Compare the payout percentages for specific injuries. A policy that pays 100% for paralysis is better than one that doesn’t cover it at all.

- Exclusions: Read the list of what’s not covered. If you’re a passionate scuba diver, make sure you find a policy that doesn’t exclude it.

- Time and Cause Limitations: Check the window of time between the accident and the loss (death or dismemberment). Most policies require the loss to occur within a specific period, such as 90 or 365 days.

Expert advice: Often, for a slight increase in your monthly premium (e.g., $15-$25), you can add $100,000 or more to your term life policy. This extra coverage protects your family from any cause of death, not just accidents, offering far greater value and peace of mind. Compare this cost directly to the AD&D premium.

The bottom line

Accidental death and dismemberment insurance provides affordable financial protection in case you die or suffer loss of critical function due to an accident. While not a replacement for life insurance, AD&D coverage is an inexpensive way to supplement existing policies.

With proper planning, this insurance can provide added peace of mind that your family will be taken care of financially in the unfortunate event of an accidental death or disability.

FAQs on Accidental Death and Dismemberment

Why is AD&D coverage affordable?

AD&D only covers accidents so there is less risk to insurers. This allows them to offer coverage at a lower premium cost than regular life insurance.

When does my AD&D coverage end?

AD&D coverage ends if you stop paying premiums or reach the age cap specified in the policy. End age varies by insurer and plan design. Some workplace plans end at retirement/age limits (often 65), while some individual accident plans may be available to older ages (e.g., Canada Life cites accident coverage options up to age 85 for certain products).

Do AD&D benefits get taxed?

No, AD&D insurance benefits are not considered taxable income. Your beneficiaries get the full amount tax-free.

Is AD&D worth it if I have life insurance?

It can provide supplemental coverage for accidents at a low cost. This is especially useful for those in risky occupations who want extra protection.

Does AD&D cover death from drug overdose?

Most policies exclude death due to the voluntary use of non-prescription drugs. Accidental overdoses may be covered if clearly unintentional.

Where can I buy individual AD&D insurance?

You can purchase individual AD&D insurance directly from companies like Sun Life, Canada Life, and RBC Insurance. Rates are higher than group plans.

Article Sources:

To ensure the accuracy and authority of this guide, we reference information from leading industry and government bodies.