Sorting out bank accounts when a loved one passes away can be a complicated task, especially if clear instructions were not left behind. It’s essential for surviving relatives to thoroughly understand what happens to Canadian bank accounts after someone dies, to close accounts and access funds properly.

This guide provides a clear, step-by-step explanation of how to handle a deceased person’s bank accounts, ensuring you can navigate this process with confidence.

First Steps: What to Do Immediately

Before any accounts can be settled, the executor or next-of-kin must take a few critical first steps:

- Locate the last will: This legal document is the cornerstone of the estate settlement process. It names the executor, the person responsible for managing the estate, and outlines the deceased’s wishes for how their assets, including bank funds, should be distributed.

- Obtain the Official Death Certificate: A death certificate is the official proof of death required by banks and government agencies. You will need multiple original or certified copies.

- Notify all financial institutions: Contact every bank where the deceased held an account as soon as possible. This notification allows the bank to secure the accounts to prevent fraud and begin the process of transitioning them to the estate.

The following sections will explore what happens to bank accounts after death in detail for different scenarios.

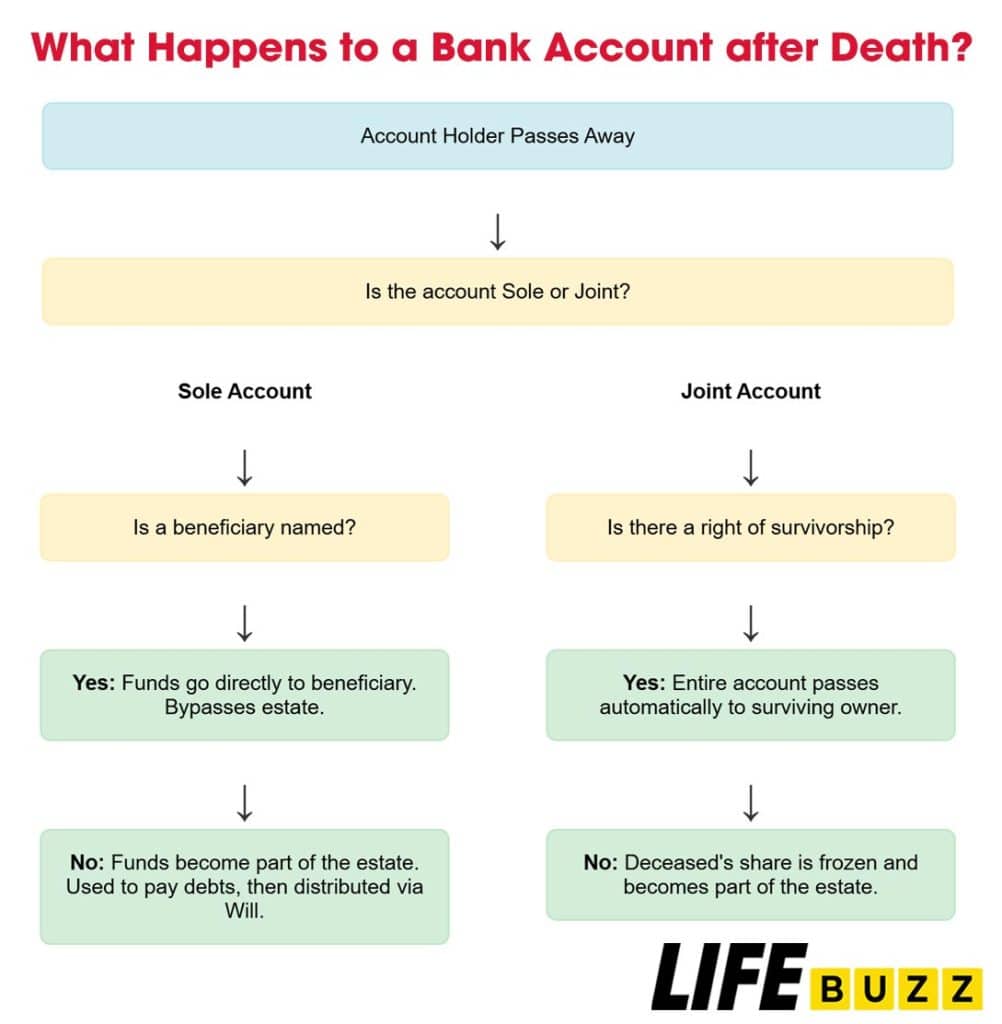

What Happens To a Sole-Owned Bank Account After Death?

For bank accounts with only one owner, there are two main possibilities after the account holder dies – the funds can either go directly to a named beneficiary or be handled by the executor of the deceased’s estate as part of the probate process. The outcome depends primarily on whether or not the original account holder designated a specific beneficiary.

If the Account Has a Named Beneficiary

Many banks allow customers to name a beneficiary who will inherit the contents of a bank account upon the original owner’s death. This type of account is sometimes called a “payable on death” or POD account. Many registered accounts, like Tax-Free Savings Accounts (TFSAs) and Registered Retirement Savings Plans (RRSPs), offer this as well.

Upon presentation of a death certificate, the funds in these accounts are paid directly to the named beneficiary, bypassing the estate and the probate process entirely. This is the fastest and most straightforward way for funds to be transferred. Once the transfer is completed, the bank typically closes the account permanently.

If No Beneficiary is Named

If no beneficiary is designated on a sole bank account, the money in the sole-owned account becomes part of the deceased’s estate and can’t be directly released. The account will be frozen, and the funds can only be accessed by the legally appointed executor or estate administrator.

The executor becomes responsible for utilizing the money remaining in the deceased’s sole bank accounts to repay any outstanding debts, with the remainder distributed to the heirs according to the instructions in the Will. Without a named beneficiary or a clear will, the probate court judge will appoint an administrator to divide the assets in accordance with the province or territory’s intestacy succession laws. In this case, accessing bank funds can be delayed for months until the probate process is fully completed.

What Happens To Joint Bank Accounts After Death?

Joint bank accounts, common among spouses and common-law partners, operate differently after a bank account holder dies compared to sole accounts. Most joint accounts include a special provision called the “right of survivorship” that affects what happens when one owner passes away.

How Right of Survivorship Works

The right of survivorship is the standard for joint accounts between married spouses in Canada (outside of Quebec), which grants the surviving partner automatic access and ownership of a shared account when their co-signing spouse dies. With this provision, the bank account does not need to be closed, does not become part of the estate and is not subject to probate.

Joint accounts between spouses typically have the right of survivorship automatically unless indicated otherwise. However, bank account holders should still double-check with their bank and make sure proper documentation was signed when the account was opened.

Even with this right, the surviving partner must notify the bank and provide a death certificate. Some banks may place a temporary hold on the account until documentation is processed, even if a right of survivorship is in place, so prompt notification is key to ensuring uninterrupted access.

What Happens if Joint Accounts Don’t Have Right of Survivorship?

A joint account may not have the right of survivorship if:

- Joint account holders are not married spouses

- The account is held in Quebec (which prohibits rights of survivorship by law)

- Owners opted out of the right of survivorship

In this case, the deceased’s ownership share of a joint bank account does not automatically transfer to the surviving account holder. Instead, the account is frozen as soon as the bank receives notice of an owner’s death. The deceased’s portion of the account becomes part of their estate and must go through probate, the same as with a sole account. An executor will utilize the portion of the joint account funds to settle any debts and distribute the remaining amount according to the will’s instructions.

The Importance of a Will When Sorting Bank Accounts

When someone dies without a will in place, it complicates the handling of the deceased’s bank account funds. Without a will to specify exactly how bank account assets should be divided after death, provincial or territorial intestacy succession laws automatically come into effect and determine who inherits the money.

A court will appoint an administrator (or estate trustee) to manage the estate. Once appointed, the estate trustee distributes bank account funds and all other estate assets based on each province or territory’s unique hierarchy of heirs.

While intestacy laws vary across Canada, the following heirs typically receive priority:

- Surviving married spouse – Receives full or majority share, especially if children are also shared heirs.

- Children – Remaining funds are divided equally amongst living children after the spouse’s share.

- Parents, siblings, or other relatives – Further distribution if no surviving spouse or children.

Without a will, distant relatives may end up benefiting partially from bank account funds, while closer friends or common-law partners receive nothing. Having an up-to-date will prevent complications and ensure account funds go where the deceased wishes.

How to Notify the Bank of an Account Holder’s Death

Before any transfers or distribution of bank account funds can begin, the deceased’s financial institutions must first be notified and verified of their death. This section covers the most common ways banks first learn that an account holder has passed away.

Notification from the Family

The executor or a close family member provides the bank with a death certificate. This is the most direct and fastest method.

The bank can then formally convert the deceased’s accounts into estate accounts and properly freeze or close them, depending on the type of account. Without the death certificate and estate documentation, banks will not release funds.

Notification from the Government

Aside from direct notification by the surviving family or associates, banks will also eventually learn of a customer’s death after the government suspends benefit payments.

For example, when someone who receives monthly Social Security payments dies, the Social Security Administration is informed of their passing and suspends future benefit deposits. This cessation of payments serves as a flag to the bank that the account holder has passed away.

An executor may also directly report a death to the Canada Revenue Agency when filing a deceased person’s final tax return. The CRA then notifies federal agencies like Veterans Affairs Canada, which, in turn, communicates with banks holding accounts for their benefit recipients.

A Practical Checklist to Make The Process Simpler

Given the complexities that can arise after death, what steps can account holders take to make the process less complicated? The following planning tips can help avoid complications and ensure bank accounts are addressed smoothly:

Designate Named Beneficiaries

One of the best ways to provide clarity on sole bank account funds is to designate beneficiaries directly. As covered earlier, this allows those beneficiaries immediate access to the money upon the original owner’s death since the bank can release it straight to them.

It also provides certainty if disputes arise over other assets, as beneficiaries legally take precedence over the named accounts. An account holder can easily change or add beneficiaries later if circumstances change.

Create a Legal Will

As we already know the importance of a will in estate planning, creating a legal will is strongly advised for all adults, especially homeowners or those with children. This central document provides definitive guidance on how all of one’s assets should be handled after death. Without a will, bank account funds may go to unintended heirs.

Consolidate Accounts

Those who handle an estate often struggle to identify all the financial accounts held by the deceased. To assist executors, account holders can take steps to consolidate accounts prior to death.

Closing extraneous bank accounts streamlines the paperwork survivors must complete with each institution. It also reduces the chance of funds being stranded in obscure accounts that heirs never uncover.

Banks may transfer dormant accounts with small balances to the Bank of Canada after set periods, forcing heirs to apply for the return of those assets. Consolidating provides clarity and avoids this issue.

Add Joint Account Holders

Married couples can simplify joint account access after death by ensuring their accounts are properly registered with rights of survivorship. Unmarried couples could consider making accounts joint instead of sole if they wish the partner to retain use of the funds after one dies.

For some accounts, account holders may provide specific loved ones with limited account access prior to death using the power of attorney documents or naming them as a secondary joint holder. This authorizes assisting with bill payments as needed if health fails.

Communicate Intentions

In addition to making legal arrangements directly with banks, account holders should communicate their wishes regarding bank account funds to family members while they are alive and competent.

Discussing intentions for distributing any sole accounts not jointly held. Sharing where documents like wills and powers of attorney are stored. Providing these details openly to heirs and beneficiaries will avoid misunderstandings.

Ensuring proper planning well in advance is the key to simplifying bank account closures after death.

Are There Tax Implications for Transferred Bank Accounts?

While Canada does not have an inheritance tax on assets like some countries, there can still be tax considerations when bank accounts change hands after death:

- Bank interest earned up until the date of death must be reported on the deceased’s final tax return if that income has not yet been declared.

- RRSPs and other registered accounts are taxable when transferred to heirs outside of transfers between qualifying spousal accounts.

- Beneficiaries who receive non-registered investment account proceeds may face capital gains taxes if the value increases.

- Consult a tax professional when managing significant account transfers.

Executors and account heirs should consider potential tax implications when closing accounts.

What Should Be Considered for Specific Account Types?

While this guide focused on typical personal checking and savings accounts, the death of an account holder can be more complex for certain assets, like:

Registered Savings and Investments – If the deceased’s RRSP, RRIF, or TFSA funds are being transferred to a surviving spouse or partner, special spousal rollover rules apply to defer taxes. For other beneficiaries, registered funds face taxation upon payment out.

Business Accounts – The death of a sole proprietor can be very disruptive for active companies, making succession planning critical. Partnership agreements dictate business account changes. For corporations, shares transfer to heirs.

Estate Accounts – Banks may open special short-term estate accounts where an executor deposits funds for bill payment until probate concludes. These simplify money management during asset distribution.

Foreign Accounts – Death procedures for accounts held in other countries vary. Taxes or court processes may differ. Legal counsel may be needed.

Understanding how bank accounts are handled after death is a vital part of estate planning and settling a loved one’s affairs. Including clear instructions in will can help avoid complications and ensure your wishes are followed. Explore more articles on this topic:

- DIY Will Kits and Templates

- Government Funeral Assistance

- Writing a Heartfelt Condolence Message

- How To Find An Obituary For A Specific Person in Canada

Summary

Given the complex legal and tax issues that can arise, it’s best for account holders to take proactive steps well ahead of time to make the handling of bank accounts after death as smooth as possible. Having clear beneficiary designations and legally valid, up-to-date wills in place can help avoid delays, confusion, and family disputes down the road.

While challenging, being aware of the key steps and documents involved after death, whether it’s a sole or joint account, ensures families properly close accounts and distribute funds according to the deceased’s wishes. Banks ultimately require standard forms like death certificates and wills before accounts of the departed can be closed out and the remaining funds released to rightful heirs or beneficiaries. A little advance planning goes a long way toward easing the burden for those left behind.

FAQs About What Happens To Bank Accounts After Death In Canada

How long does it take for a bank to release funds from the account of a deceased person?

Banks typically release funds from a deceased person's account within 1-4 weeks after receiving the required death certificates and paperwork from the estate executor or administrator. However, the entire process, including getting probate, can take several months.

What happens if government payments go into the account after death?

You must return any funds deposited after the date of death (e.g., CPP, OAS, Social Security) to the government. Keeping them is considered fraud. Notify the issuing agency and the bank immediately.

Can a bank place a hold on the account of a deceased person?

Yes. Upon notification of death, banks will freeze sole-owned accounts to protect them. They may also place a temporary hold on joint accounts until a death certificate is provided.

Do all bank accounts get closed after death?

Sole accounts will be closed, while joint accounts with a surviving owner typically remain open and transfer to the survivor. Special estate accounts may also be opened by a bank's trust department to aid the executor.

What happens to safety deposit boxes after death?

The contents will be inventoried by the bank in the presence of the executor/administrator before assets are released. Some states allow spouses to access jointly held boxes automatically.

Who pays any outstanding debt on the credit card of the deceased?

Generally, the estate of the deceased is responsible for paying off credit card balances unless someone else is jointly liable for the account. The executor uses estate assets for debt repayment.

How does a bank know if a Will is legally valid?

The bank will only honour a will that has been submitted to probate court and received confirmation of executor appointment in certified court documents.