“What happens when your term life insurance policy expires?” This is a common question when purchasing term life policies in Canada. While this type of life insurance provides affordable protection for a period of 10 to 30 years, it is temporary and only pays out if you pass away during the term. If you take no action, your coverage will end at the end of the term.

So, what to do next? In Canada, you have four primary paths you can take: renew, convert, allow your policy to lapse, or apply for a new one. Making the right choice depends on your current health, financial situation, and future needs. This guide will explain each option in detail to help you make an informed decision.

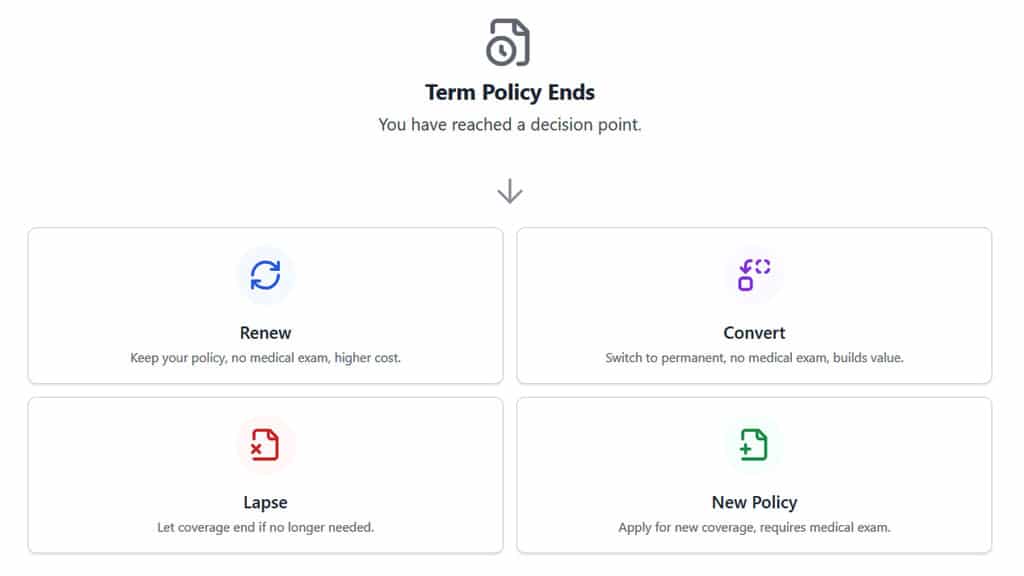

Option 1: Renewing Your Existing Term Policy

Some Canadian insurers allow you to renew your coverage for another term up to a certain age, typically 75 or 80. You simply continue paying premiums to keep your coverage active.

The most significant benefit of renewal is that no medical exam is required. If your health has declined since you first bought the policy (e.g., you’ve been diagnosed with a chronic illness, had a heart attack, or developed diabetes), renewal may allow you to maintain your coverage.

However, premiums will be significantly higher than your original policy since the renewal premium will be based on your current age. It is not uncommon for a monthly premium of $60 to jump to $500 or more upon renewal.

Who should consider this? Individuals whose health has significantly worsened, making it difficult or impossible to qualify for a new, medically underwritten policy.

Option 2: Converting to Permanent Life Insurance

Many term policies also include a “conversion privilege” or “conversion option.” Rather than renewing for a fresh term, you have the option to convert your term coverage into a permanent life insurance policy before it expires, without a medical exam. This is invaluable if your health has changed.

Permanent policies do not expire as long as you pay the premiums and can also accumulate a “cash surrender value” on a tax-sheltered basis. This becomes a financial asset you can borrow against or withdraw from later in life.

One thing to consider is that premiums for permanent life will be higher than your term policy. However, the premium will be lower than if you were to apply for a new permanent policy from scratch at your current age.

Important note: You must exercise this option before a specific deadline, which is often before the term expires or before you reach a certain age (e.g., 65 or 70). You choose a permanent plan offered by your insurer, and your premiums adjust to the new rate.

Who should consider this? Those who have developed health issues and have a lifelong insurance need, such as for estate planning, covering final expenses, or leaving a tax-free inheritance.

Option 3: Let The Policy Lapse

This is the simplest option: do nothing. When the term ends, you stop paying the premiums. The policy lapses, and the insurer is no longer obligated to pay a death benefit

When is this the right choice? This is a valid strategy if your financial needs and dependents have changed such that you no longer require life insurance. For example:

- Your mortgage is paid off.

- Your children are financially independent adults.

- You have accumulated enough savings and investments to be “self-insured,” meaning your spouse or dependents would be financially secure without an insurance payout.

Note: Ensure you carefully evaluate your ongoing insurance needs before letting the policy lapse so you do not become uninsured later on. Once coverage lapses, you cannot restore it without a new application.

Option 4: Apply for a New Policy

This option is often overlooked. If you are still in relatively good health, you can shop the open market for a brand-new policy. You will need to complete a new application and undergo full medical underwriting, which may include a questionnaire, a nurse’s visit, and fluid samples.

The major advantage is cost savings. If your health is the same or better than when you first applied, a new, fully underwritten 10 or 20-year term policy will almost always be cheaper than renewing your old policy. Competition between insurers works in your favour.

However, you need to be qualified. If your health has deteriorated, you may be denied coverage or offered a much higher premium than expected. This is why it is wise to explore this option before your current policy’s conversion and renewal deadlines pass.

Who should consider this? Anyone who is still in good health and has an ongoing need for affordable, temporary coverage.

Strategic Planning at the End of Your Term Life Insurance

When purchasing term life insurance, it’s essential to consider your needs at the end of the term period. Here are some planning tips as your policy approaches expiration:

Consider Your Future Insurance Needs

Do you still need life insurance coverage? And for how many more years?

Your agent can help analyze this as your term policy ends. Ensure you account for any mortgage, college costs, income replacement, and other expenses your beneficiaries may face.

Review Options with Your Agent Before Expiration

A few months before expiration, meet with your agent to discuss your options – renewing, converting, or letting the policy lapse. They can explain the features and costs of each choice. This ensures you make an informed decision when the time comes.

Do Not Let Your Policy Lapse Unintentionally

Mark your calendar well before the expiration date so you have plenty of time to plan. Pay close attention to any renewal or conversion deadline notices from your insurer. You want coverage to stay intact simply because you forgot to take action.

The Bottom Line: Be Proactive

The expiration of your term life insurance policy is not an end, but a transition point. By understanding your four key options and planning ahead, you can ensure your decision aligns perfectly with your family’s current and future financial security.

FAQs

Can my insurance company refuse to renew my policy?

No. If your policy contains a “Guaranteed Renewable” clause, the insurance company is contractually obligated to let you renew your coverage without any medical questions. However, they are not obligated to offer you the same premium; you will have to pay the higher, age-adjusted rate.

Do all term policies in Canada have a conversion option?

No, not all of them do. While the conversion privilege is a very common feature, some lower-cost or simplified-issue policies may not include it. Review your original policy documents or speak with your advisor to confirm whether you have this option and the deadline to exercise it.

Can I convert just a portion of my term policy?

Yes, in most cases. This is known as a partial conversion. For example, if you have a $1,000,000 term policy, you could choose to convert $250,000 to a permanent policy for final expenses and estate needs, while letting the remaining $750,000 of term coverage expire. This can be a flexible and cost-effective strategy.

Can I get any money back if I let my policy lapse?

No. A standard term life insurance policy has no cash value or investment component. You are paying purely for the death benefit protection over a set number of years. If you don’t pass away during the term, the policy expires without any refund.